AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Returning home from a recent holiday in Bali, I tried to pay for groceries using a Visa card, only to have the transaction declined for a lack of funds. Putting aside the embarrassment of holding up a long line of customers at the checkout, I logged onto my bank's app to figure out why the card was declined, as the card had plenty of funds the last time I checked.

The statement showed two pending transactions totaling just under $3,000 each, from an unnamed merchant, identified only as a random series of numbers and letters. I called my bank and was informed that both transactions were made that day from the same merchant in Indonesia. After explaining that we had recently returned home, and the transactions couldn't be mine, I was informed that my card was (most likely) skimmed while we were in Bali and would need to be canceled.

Skimmed? What's that? Let's look at the answer and how to prevent credit card fraud while traveling.

Page Contents

So, What Is Credit Card Skimming?

Card skimming is an illegal method of capturing personal banking information for use in credit card fraud and bank fraud, and it is BIG business.

Skimming occurs when devices illegally installed on ATMs, point-of-sale (POS) terminals, or fuel pumps capture data or record cardholders' PINs. Criminals then use the data to create fake debit or credit cards and then steal from victims' accounts. Here are some statistics to keep in mind as we continue roll into 2024 and an ever-growing digital age:

- Credit card and debit card fraud projections for 2024 estimate that the total losses worldwide will eclipse $43 billion. This figure is up from $9.84 billion back in 2011 and $32.4 billion in 2021.

- Cumulative losses in online payments due to fraud are expected to amount to $343 billion for merchants between 2023 and 2027.

- 42% of all e-commerce fraud (by value) occurs in the U.S. 26% is in Western Europe and 22% in Asia.

- Debit card fraud is less common than credit card fraud. Just 17% of cases were tied to a debit card, resulting in $117 million lost in a single year.

- Card issuer losses occur mainly at the point of sale from counterfeit cards, while merchant losses occur mainly on card-not-present (CNP) transactions on the internet, at a call center, or through mail order.

(Source: Merchant Savvy, February 2024)

To put credit card fraud in perspective, Iceland's estimated GDP is $17 billion. Credit card fraud worldwide will be more than double that this year; these are big, global numbers.

There are four primary ways identity thieves can skim your card.

- At an ATM: Using an overlay on the card reader, the magnetic strip is scanned as the card goes in and out and PINs are recorded — either via camera or pressure-sensitive keypads.

- During a purchase: Information is typically harvested using card readers at the point of sale. This method is declining in popularity with the introduction of EMV secure chips but is still prevalent in the U.S., Asia, and Eastern Europe.

- Contactless payments: Using mobile point-of-sale machines, all an identity thief needs to do is pre-set a sale of $30 or $40 into the terminal, place it in a bag, and walk around bumping into people's back pockets and bags.

- Online: Still the most widespread credit card fraud (and typically not the result of user error). The majority of credit card details obtained online are from hacked e-commerce merchants or breaches from the processor or network handling online payments.

And while there are multiple ways identity thieves can get your credit or debit card details, there are also several ways you can prevent yourself from becoming a victim of identity theft. Below we've put together 9 tips on how to prevent credit card fraud when traveling.

How To Prevent Credit Card Fraud When Traveling

Charge to your room

When staying in a hotel or resort, charge everything to your room and pay the total at checkout. It may sound overly simplistic, but you are much less likely to be targeted at the reception desk of a busy hotel with a reputation to protect, where your card is in sight, than you are handing your card to a pool attendant to process at the bar. Don't let your card out of your sight!

Use an app to put a ‘hold' on your card

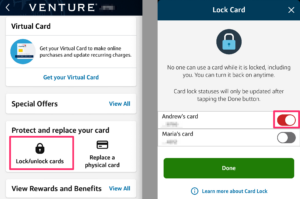

Try using a card that can be locked or switched on and off via your computer or phone. Some third-party apps have this functionality, but check with your bank first. For example, my Capital One Venture Rewards Credit Card has a hold button in-app that locks further use of the card until I take it off hold — again done via the app. The caveat is that you can't unlock the card if your phone dies or you don't have an internet connection. Discover offers something similar, as well, where you can freeze your Discover account.

Prepaid debit cards

Loading money onto a prepaid debit card for purchases while abroad can prevent your primary credit card details from being scanned. Revolut offers members the chance to grab one of the best international prepaid Visa debit cards that can hold up to 30 different currencies to be spent in over 150 different countries. One of the great features of this card is that it allows you to waive currency exchange fees to convert your home currency to the local currency of your travel destination on the first $1,000 per month. You'll also be able to withdraw cash from ATMs worldwide without incurring fees (up to a $1,200 limit monthly). After that $1,200 limit, each withdrawal will incur a 2% fee. This is quite generous when you consider that Revolut's chief competitors only have a $250 monthly limit.

Secondary accounts

On a recent trip to Asia, we opened a separate checking account with our bank and had a Visa debit card attached to the account. When we wanted to use the card to pay for anything or to withdraw cash, we only transferred the exact amount we needed into the secondary account from our primary account via the bank's app. This way, the account connected to the card remained empty unless we needed immediate access to the funds.

Geolocation software

Although not widely available yet, some financial institutions will pair geolocation software with your card on request. Paired with your phone, if the phone and the card are not in the same location, the transaction won't process. The downside is when you accidentally leave your phone in the hotel, or it runs out of juice, you can't use the card. Give your bank a call to see if this service is available. It's a fantastic security feature.

EMV security chips

Use a card with an EMV security chip like the Chase Sapphire Preferred® Card. Most new merchant card terminals have a slot to accept credit and debit cards equipped with an EMV security chip. The reason cards with a magnetic strip are so susceptible to credit card fraud is the data contained in the strip never changes. EMV secure chips, on the other hand, produce unique, single-use tokens that are impossible to predict and cannot be reproduced by hackers. The tokens are only good for one transaction.

Note: EMV technology doesn't work when using an ATM or when using the swipe functionality at a point-of-sale terminal.

Cash

Cash is still king in many parts of the world. During our two months in Indonesia, there were neither ATMs nor card terminals for miles in any direction on multiple occasions. At these times, it was necessary to withdraw a significant amount of cash. When withdrawing money from ATMs, look for ATMs inside bank foyers and hotel receptions — preferably places with security guards. These machines will be inspected daily and are much less likely to be targeted; you are most at risk of card skimming when using ATMs in bars, gas stations, and convenience stores.

Virtual account numbers

Protecting yourself online, particularly when using offshore websites not subject to U.S. laws, is surprisingly easy. Virtual account numbers from Capital One and other banks will generate a temporary credit card number, expiry date, and security code that can only be used for one transaction. Some third-party vendors are providing a similar service through E-wallets like AlliedWallet. If your bank offers this service, it should be your first stop when thinking about how to prevent credit card fraud when shopping online.

RFID protection

As contactless payment becomes more popular, so does the use of wireless skimming technology. Nearly all financial institutions offer security promises and money-back guarantees in the case of fraud, but I believe it's far better to take the lead in protecting yourself from identity theft. RFID-blocking wallets like the Access Denied Men's RFID Blocking Wallet protect your information against skimming from wireless devices. Alternatiely, choose a more robust solution like Amourcard, which actively jams nearby radio frequency signals. You can also DIY a cheaper handmade solution by wrapping your cards in aluminum foil which, according to science (and my Dad), has nearly the same effect.

Final Thoughts

Having spent a good portion of the last 16 years traveling and the last year on the road in Asia, I considered myself fairly savvy about how to prevent credit card fraud…until someone withdrew almost $600 from my account without me knowing. The loss of a few hundred dollars was a nuisance, but having to cancel and cut up my cards (my rep from the bank recommended canceling every card I used in Indonesia) was a hassle.

While this list doesn't cover every solution to protect yourself from credit card fraud while traveling, implementing as many of these as you can makes the jobs of would-be thieves much harder.