AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Have you ever been shopping online and been given the option to delay or break up your payments? These options are everywhere — whether you're at Walmart, Target, or one of the thousands of other retailers that offer buy now, pay later financing.

But, using any of the “buy now, pay later” programs you'll find advertised on different websites is rarely a great idea. Here's a look at what buy now, pay later is and when it is — and isn't — a good idea to use these services.

Page Contents

What Is Buy Now, Pay Later?

Maybe you've hit the checkout screen when shopping, only to be overwhelmed with a veritable buffet of different payment methods. These often include buy now, pay later offerings. And this usually includes popular companies such as Klarna, Afterpay, Affirm, Sezzle, and Splitit. (We promise we didn't make any of those names up.) Other options include equal monthly payments through Amazon Pay when paying at thousands of merchants online.

If you're a frequent online shopper, these will likely look familiar. Buy now, pay later companies are the online answer to in-store financing. They work similarly: You make a purchase, (usually) apply for credit, and take your time making payments on what you've bought.

In theory, it's pretty simple. And it can seem incredibly enticing if you're making an expensive purchase. However, using this type of financing is rarely a good idea since it can cost a lot more in the long run.

When You Should Use These Programs

Before discussing the negative aspects of buy now, pay later programs, let's consider when they can be beneficial.

If you can pay off your purchases quickly and at no extra cost

Using a buy now, pay later financing program won't always cost extra. Many of these programs provide interest-free options, provided your credit is good and you are looking at a short-term option.

For example, Afterpay will routinely offer an interest-free four-payment option. This means if you pay the total purchase price within four months, you will pay no extra interest or fees.

If you need to alleviate the burden of a large purchase

We don't recommend carrying a balance on a credit card or a personal loan. But sometimes things happen, and we aren't always prepared. Say your heat pump goes kaput, winter is around the corner, and you don't have the money saved to replace it. In these emergencies, buying now and paying later financing can be a lifesaver.

In this instance, buy now, pay later financing can potentially be less expensive than other types of debt. This is especially true with credit cards.

Let’s say you’re in an emergency and need to decide between carrying a balance on a credit card or using something like Afterpay. The best rewards credit cards often charge high interest rates. But if you apply for one with a 0% APR introductory offer, it might let you defer payments without cost. These cards can give you time to pay off the balance without accruing interest, helping you save money while managing the expense.

When you want to build your credit

If you have a limited credit history and want to build your credit, using a company such as Klarna for your purchase can help. This is because it can report payments to the credit bureaus. Making on-time payments and paying off the loan can help you establish a positive credit history.

However, not all impacts on your credit will be good — especially over the short term. Read more about this in the downsides section below.

Downsides of Using Buy Now, Pay Later

What are the reasons to avoid buy now and pay later options? There are several.

You may end up spending more than you can afford

One of the most important rules of credit is paying everything off monthly when possible. This is especially applicable to those chasing points and miles because interest rates on travel credit cards are typically higher than average.

This same rule applies to anyone choosing buy now, pay later financing. In most cases, you never want to buy something and pay it off over a longer period of time. It's easy to overspend on things you can't afford when the costs are broken into smaller monthly payments.

Interest and fees make your purchase more expensive

Depending on your financing option, buy now, pay later purchases will incur two different costs: interest or monthly fees. Interest accrues on your balance and adds to your total each month. Monthly fees are fixed and are tacked on to your plan each month. Either way, you're paying more for your purchase than you would have had you paid in full outright.

Taking time to pay off your purchase could open you up to paying more fees. If you struggle to make timely payments, this could greatly impact your finances. Late payment charges can stack up, adding even more to the final tally of what you owe.

Your credit score may be impacted negatively

Most buy now and pay later companies rely on your credit score to determine whether or not to lend you money. Understandably, these companies would want to check your credit before lending you money. But keep in mind this could cause your credit score to drop.

Hard inquiries are created when a lender checks your credit score and are considered a negative mark on your credit. It's not permanent, but it will more than likely lower your credit score for a few months. Also, having too many of these on your account can significantly lower your score as it indicates that you're applying for a lot of new credit. This is a worrying sign to future lenders.

Buy now, pay later financing can also be a mixed bag when reported to credit bureaus. Some companies, such as Afterpay and Affirm, don't usually report anything to your credit report. However, some buy now, pay later options will appear on your credit report — for better or worse. If you don't already have a lot of credit, adding a new debt can cause your score to fluctuate drastically.

Fees and interest can negate the value of credit card rewards earned

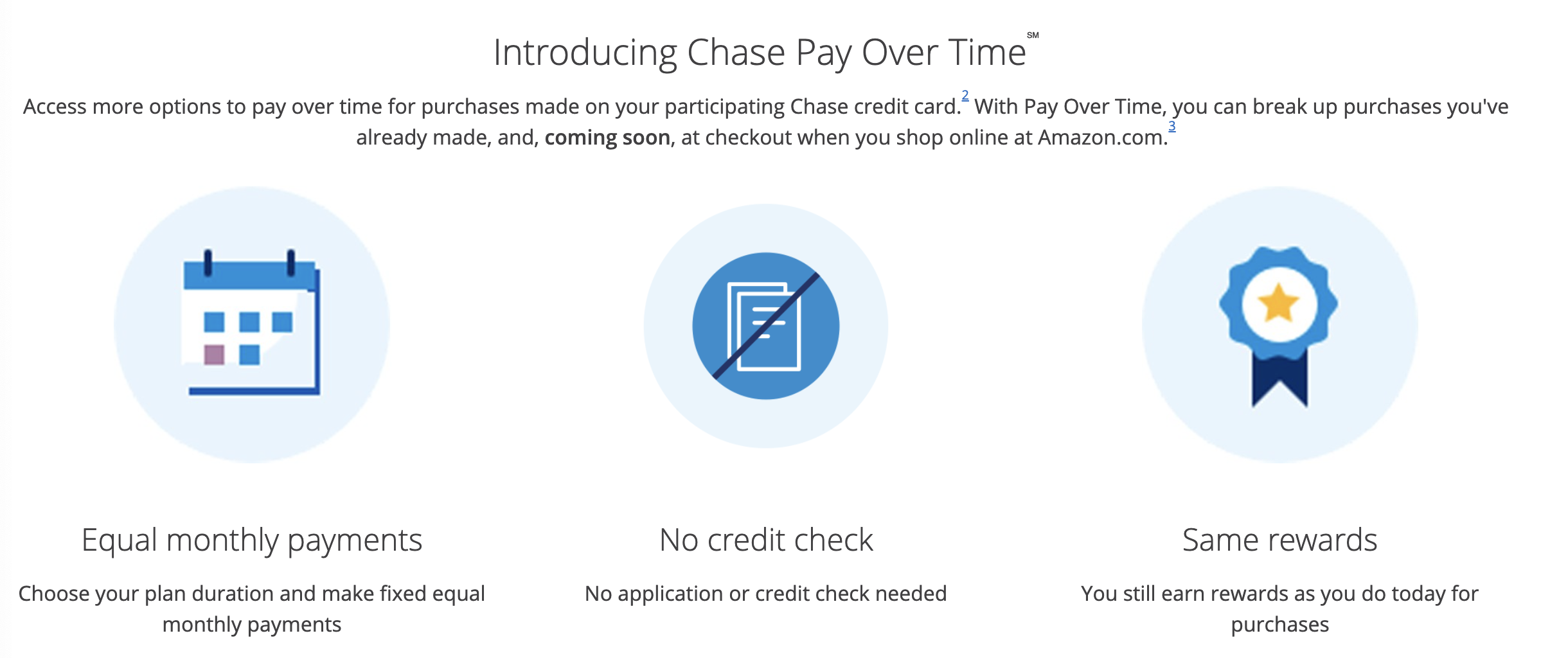

Card issuers such as American Express (via Amex Pay Over Time) and Chase (via Chase Pay Over Time℠) will offer buy now, pay later options to cardholders. However, this option is still typically not worth it. While you're using a credit card that earns rewards, you'll be able to get points and miles for your purchases — but at what cost?

Let's say you've used the Chase Sapphire Reserve® to book a flight for $1,000. You'll earn 4X Ultimate Rewards on your purchase for 4,000 points in your pocket. AwardWallet users tend to redeem Chase points at 2.01¢ apiece, which means those 4,000 points can be worth nearly $80.

Chase offers a buy now, pay later service called Chase Pay Over Time, which allows you to make monthly payments at a fixed rate. Between earning rewards and being able to defer payments, it's easy to upgrade to a more expensive flight option. Plus, if you're charged more than approximately $60 for the fees associated with Chase Pay Over Time, you're wiping out the value of any rewards you've earned.

Bottom Line

Buy now, pay later financing can be tempting when making purchases. However, you should resist the urge, especially since many downsides exist. There may be a few instances when this type of financing makes sense, such as emergencies or special offers to defer payments at no extra cost. However, these are the exception rather than the rule.

Otherwise, buy now, pay later options aren't a good option. These options cost more, can negatively impact your credit, and can wipe out any points or rewards earnings you'll get on a credit card. Do yourself a favor and pass them by.