AwardWallet may receive compensation from advertising partners when you visit our site, click on a link, when you are approved for a credit card, or when an account is opened. Terms Apply to the offers listed on this page. Enrollment is required for select Amex benefits. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here’s our complete list of Advertisers.

If you've ever rented a car before, you're probably familiar with the hardcore upselling agents will use to get you to purchase their insurance. Whether they insist that it's mandatory or speculate about improbable car accidents, these high-pressure tactics are unpleasant — and often unnecessary. This is especially true if you hold a variety of travel credit cards, many of which offer complimentary rental car insurance. But when that's not enough, American Express Premium Car Rental Protection comes to the rescue.

Available to eligible Amex cardholders, this rental car insurance allows you to decline those pesky salesmen with confidence. Let's take a look at American Express Premium Rental Car Protection, what it covers, how much it costs, and whether it's worth the fee.

Page Contents

- What is Amex Premium Rental Car Protection?

- Which Cards Offer Amex Premium Car Rental Protection?

- What Isn't Included With Amex Premium Rental Car Protection?

- How to Enroll in Amex Premium Car Rental Protection

- How to File an Amex Premium Car Rental Protection Claim

- Is it Worth Getting Amex Premium Rental Car Protection?

- The Bottom Line

What is Amex Premium Rental Car Protection?

American Express' cards offer rental car loss and damage protection, but there are times where that isn't enough. In addition to limits on coverage, the car rental loss and damage insurance provided by your American Express card is secondary. This means it pay out after other options. If you have personal car insurance, for example, you're likely covered for rental cars; this would be your primary insurance. Amex wouldn't pay out until you'd exhausted your personal insurance.

In contrast, Amex's Premium Car Rental Protection is primary — at least for damage or theft of the vehicle and accidental death and dismemberment (AD&D) protection. Plus, coverage limits are higher than you'll find via the complimentary car rental loss and damage insurance on your card.

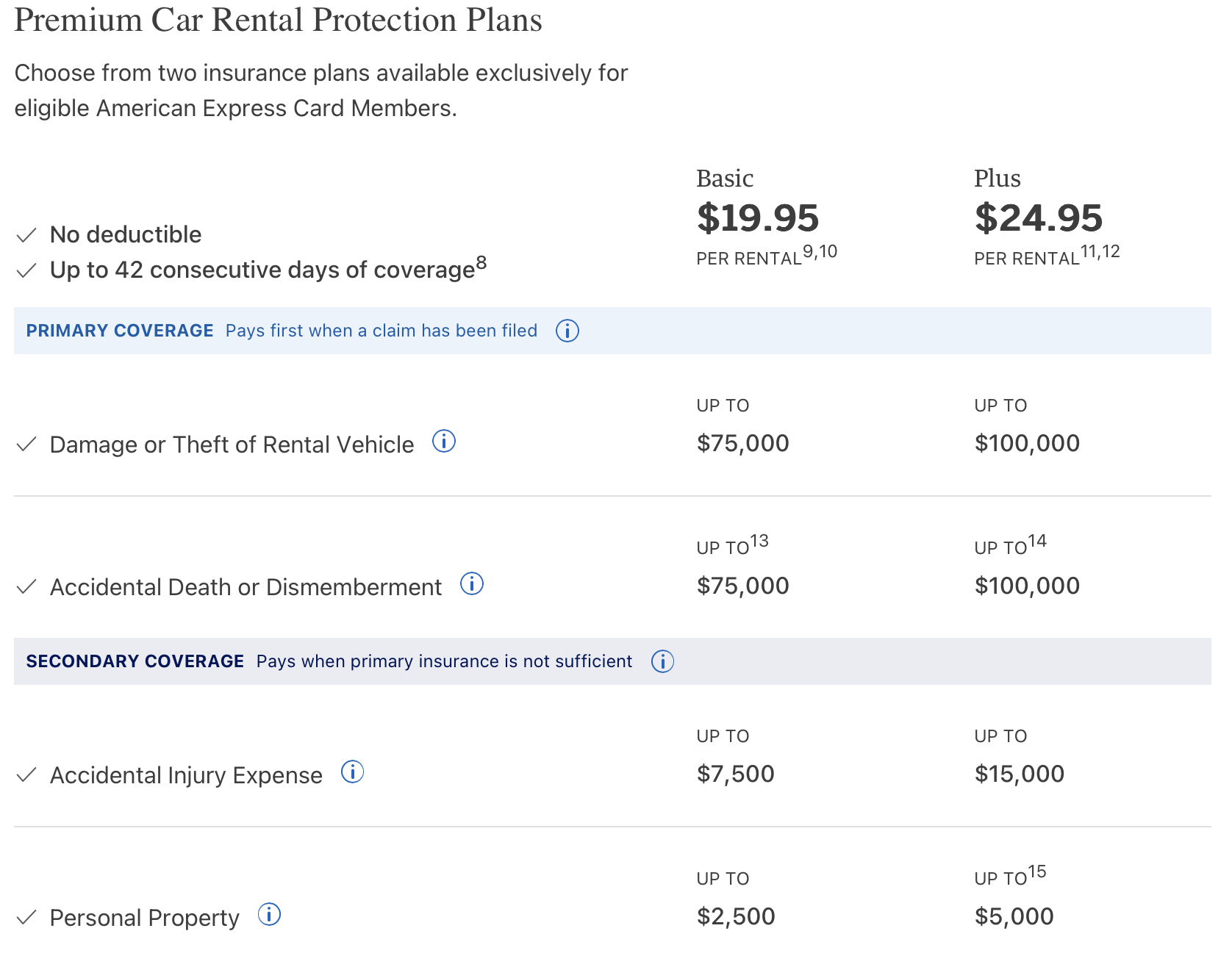

It's important to note that American Express Premium Car Rental Protection is not a free perk for holding your Amex card; it comes at an extra cost. The price is a flat rate and the amount you'll pay will depend on the plan you pick and where you live.

Here's what it looks like for most U.S. residents.

As you can see, you'll pay slightly more for higher coverage limits though no matter the plan you choose you'll have no deductible.

You're also eligible for up to 42 days of coverage in every state but Washington, which is limited to 30 days.

Once you've been enrolled in Premium Car Rental Protection, every time you rent a car and pay with your card you'll automatically be charged your flat-rate fee. You'll then be covered with this protection.

Which Cards Offer Amex Premium Car Rental Protection?

Most American Express cards can be enrolled in Amex Premium Car Rental Protection. These include:

- American Express Platinum Card®

- The Business Platinum Card® from American Express

- American Express® Gold Card

- American Express® Business Gold Card

- Marriott Bonvoy Business® American Express® Card

- Marriott Bonvoy Brilliant® American Express® Card

- Delta SkyMiles® Platinum American Express Card

- Delta SkyMiles® Reserve American Express Card

- Hilton Honors American Express Aspire Card

- Hilton Honors American Express Surpass® Card

What Isn't Included With Amex Premium Rental Car Protection?

Although Amex's Premium Car Rental Protection is pretty comprehensive, there are certain situations in which your rental is excluded from coverage, including:

- Renting custom or modified vehicles

- Vehicles more than 20 years old

- Rental originating in Australia, Ireland, Israel, Italy, Jamaica, and New Zealand

- Loss incurred during a violation of the rental agreement

- The rental being left unattended and unlocked or a window not being completely closed

As far as personal property goes, these items are excluded:

- Animals

- Furniture

- Art

- Tires

- Money

- Any items left in the car after it's been returned

How to Enroll in Amex Premium Car Rental Protection

Enrolling in American Express Premium Rental Car Protection is simple, though you'll need to log in to your account to do so. You'll then want to navigate to the Premium Car Rental Protection page or simply click here.

After you've enrolled, you simply need to pay for your rental with your American Express card. The fee will be automatically charged and coverage will commence.

How to File an Amex Premium Car Rental Protection Claim

If the worst ends up happening and you have damage to your rental car, you'll want to file a claim. To do so, visit the American Express Claims Center. Claims typically take about five to ten minutes to file if you've already got the necessary information on hand. This includes:

- Personal information

- Details of the incident

- A police report (if you have one)

- Photos of the damage

- An itemized bill for repair

- Copy of the rental agreement

Other supporting documentation may be required depending on what occurred.

Once you've filed your claim, you can check on its status by revising the claims center. It takes an average 45 days to reach a decision, though this can extend up to 60-90 days for international rentals.

Related: Skip the CDW: How to Use Credit Card Rental Insurance and Get Proof When Needed

Is it Worth Getting Amex Premium Rental Car Protection?

American Express Premium Rental Car Protection is an affordable option for American Express cardholders to get primary insurance on their rental vehicles. This is especially true when compared to the insurance that actual rental car companies try to sell you. But is it worth it?

If you already own a car and have personal insurance within the United States, odds are good that you're covered for rental vehicles. You'll want to double-check your policy to be certain, but this is the standard.

However, if you don't want to rely on your personal insurance or you're renting a car abroad, you may need to get supplementary insurance. In this case, Amex Premium Rental Car Protection fits the bill. Paying its fee increases your coverage limits and jumps your insurance from secondary to primary.

That being said, there are better options available if you're willing to apply for other credit cards. For example, the auto rental coverage included on the Chase Sapphire Preferred has a limit of $60,000, is primary, and is complimentary as long as you use your card to pay for your rental.

Related: Best Credit Cards for Rental Car Insurance

The Bottom Line

American Express Premium Car Rental Protection can be the right fit if you're looking for primary coverage on a rental car. It's fairly inexpensive and offers insurance against damage, injury, death and loss of personal property. But if you're looking to save money while still enjoying insurance, consider using a travel credit card that offers primary insurance for free.