AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Offers for the Chase Freedom Flex℠ and Ink Business Preferred® Credit Card are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

May 24 = 5/24. So naturally, we’re covering all things Chase 5/24 on AwardWallet today. Whether you’re under, over, or not sure what 5/24 even means, we’ve got guides, tips, and strategies to help you navigate this card application rule.

Among points and miles enthusiasts, few restrictions are more infamous than Chase’s 5/24 rule. However, the 5/24 rule can confuse and frustrate new entrants to the points and miles world, especially since it’s so common to find online references to “5/24 status” or being “over 5/24” without any additional context.

Most credit card issuers follow internal guidelines to determine who qualifies for a new account. While these application rules are rarely published or officially confirmed by the banks, the points and miles community has a long history of uncovering them through shared experiences and strategic discussion. Thanks to crowdsourced data points from card applicants, we've been able to piece together many of these unofficial rules.

In this post, we’ll cover everything you need to know about the Chase 5/24 rule: how it works, how to check your status, what cards are affected, and how to build a smart application strategy around it.

Page Contents

The Chase 5/24 Rule Explained

Chase will generally deny your application for a new card if you have opened five or more card accounts in the previous 24 months, thus, “5 in 24” or just 5/24. When you apply for a new card, Chase will obtain a copy of your credit report from one of the three major credit bureaus: Experian, Equifax, and TransUnion.

If your personal credit history shows at least five credit card accounts with an “opened date” in the last 24 months, Chase will generally reject your credit card application.

What Counts Toward My 5/24 Status?

The basic rule is straightforward. If it’s a credit card account and it appears on your credit report, it counts toward 5/24. But since we’re not all experts on credit reporting, here are a few things to remember.

Which cards count toward 5/24?

- All card issuers: Chase counts the credit cards from all card issuers that appear on your report, not just the ones issued by Chase.

- Even closed cards count: Closing a credit card does not remove it from your credit report. If you have opened the card within the past 24 months, it will still count towards your 5/24 status.

- Authorized user cards may count too: If you are an authorized user on someone else’s credit card account, the bank may report that account to your credit report. If so, it will count toward your 5/24 status. However, you may be able to remove it from your report. More on that below.

What credit lines don't count toward 5/24?

- Unsuccessful credit card applications do not count toward your 5/24 status. They will show as an inquiry on your report, but only new accounts that you successfully open count.

- Many business cards do not appear on your personal credit report, and therefore, they won't count toward your 5/24 status. See below for more information on the business cards that count.

- Other types of credit accounts on your credit report, such as mortgages, student loans, and car loans, do not factor into your 5/24 status.

Which Chase Cards Are Subject to Chase's 5/24 Rule?

If you're in the market for a new Chase card, it's best to assume that all personal and business cards issued by Chase are subject to the 5/24 rule. This means that any application for a Chase card will likely be denied if you have already opened five cards in 24 months.

When this restriction was first introduced, it only applied to a few specific cards. However, in 2018, Chase expanded the restriction to virtually all Chase cards — even no-annual-fee cards like the Chase Freedom Flex℠.

Are there ever exceptions? Quite possibly. Over the years, we have seen many reports of Chase credit card approvals that should've been rejections based on 5/24 status. But these anecdotal claims can be hard to verify. So, take these reports with a grain of salt.

Some have speculated that the rule isn’t always enforced for certain co-branded cards. Some suggest Chase's “Just For You” offers or those from targeted mailers might bypass the 5/24 rule. Perhaps Chase bends the rules for customers who meet specific additional criteria, such as Chase Private Client customers. Long story short, there's no hard evidence to support these claims. And without more transparency from Chase, it's tough to know for sure.

The best approach is to plan your card applications accordingly. If you're under 5/24, prioritize getting Chase cards. Then, pursue cards from other card issuers later. This way, you'll avoid rolling the dice on an unnecessary hard pull to your credit report.

Related: Chase Credit Cards: Best-Ever Offers and When You Should Apply

How Can I Check My 5/24 Status?

Chase relies on your credit report to determine your 5/24 status. You can check your 5/24 status through several free methods. Here's a quick overview of a few options.

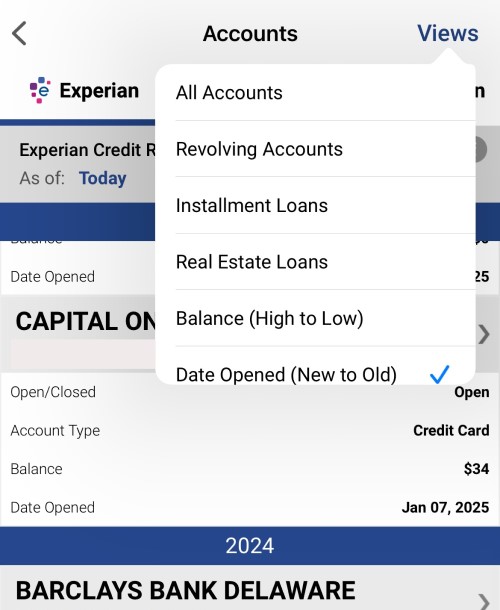

Experian

You can sign up for a free Experian account, and checking your 5/24 status on the app is very simple. Log in, and once viewing your report, click on the total accounts and sort by date opened. Count the number of listed accounts opened in the last 24 months.

Experian will try to convince you to sign up for a paid account. But remember, you don't need to pay to check your Chase 5/24 status. All you need to do is click out of the upgrade advertisement, locate your records, and Experian will display the date you opened each account.

Credit Karma

Credit Karma will show you your Equifax and TransUnion credit reports. Click on the report you'd like to view and scroll down to Credit Age. You will then see a list of your cards and the age of each account. After checking everything, total the number of credit card accounts you've opened in the past two years.

TravelFreely

Finally, the TravelFreely App, which allows you to enter your card opening dates manually, will track your 5/24 status, but of course, this requires you to enter each card as you open it. It can be a handy way to keep track without the use of a spreadsheet, but it requires a bit of legwork up front to enter all of the data.

Do Business Cards Factor Into My 5/24 Status?

If you want to apply for a Chase business card, you are still subject to the 5/24 rule. That is to say, Chase will generally not approve your application for a new business card if you're over the 5/24 limit.

However, you may have read that business cards don’t count toward 5/24. That's true for most business cards but is confusing for many. We say “most” business cards because select card issuers report opened accounts to your personal credit report.

Quick recap:

- All personal credit cards from every issuer are recorded on your credit report and count towards your 5/24 status.

- Business credit cards from Capital One, Discover, and TD Bank are generally recorded on your personal credit report. Thus, these business cards count towards your Chase 5/24 status.

- Business credit cards from American Express, Bank of America, Barclays, Chase, and Citi generally aren't recorded on your personal credit report, so they don't count toward your 5/24 status.

- Capital One says it doesn't report its business charge cards (those with no preset spending limit) to your personal credit report, so long as the account is in good standing.

Related: Am I Eligible for a Small Business Card?

How Authorized User Accounts Affect 5/24

If you are an authorized user on someone else's personal credit card account, this account will show up on your credit report and count towards your 5/24 status. Thankfully, you're not stuck with this mark on your Chase 5/24 status. You can have authorized user accounts removed from your 5/24 status in two ways.

Related: Does Being an Authorized User Affect Your Credit?

The first step is to ask the primary account holder to remove you as an authorized user. Once they do, contact the credit reporting agencies to have the authorized user account removed from your report.

Remember to only do this for authorized user accounts opened in the last 24 months. You don't need to remove older authorized user accounts for the sake of 5/24 status. Those won't affect your Chase 5/24 number; these accounts can help build your credit history.

The other option is to try working with Chase's reconsideration department after a denial. Chase card applicants have reported success in requesting that a reconsideration agent remove authorized user accounts while reconsidering their card application.

For example, let’s say you’ve opened four personal credit cards in the past 24 months and you’re also listed as an authorized user on two other accounts opened during the same timeframe. When Chase reviews your application, it will typically count all six accounts toward your 5/24 status. This means you would be considered 6/24 and likely ineligible for automatic approval. But you can ask a Chase reconsideration agent to remove the two authorized user accounts from consideration. They can quickly analyze your credit report and see that you're under 5/24.

Not everyone is going to like this method. After all, this requires applying for a Chase card with the knowledge that you'll likely be denied at first. Then, you'll need to call Chase's reconsideration desk, which is a process that some may find intimidating. And you aren't guaranteed that they will approve you. But this process is worth it for those who don't want to go through the trouble of removing authorized user accounts from their credit report.

What If I'm Already Over 5/24?

If you are already over 5/24, you have a tough decision. Should you avoid opening new personal credit cards while you wait for some of your existing accounts to age out of the 24-month timeframe?

Option 1: Wait It Out

If you're only a few months away from dipping back under 5/24, it might be smart to press pause on any new personal card applications. Holding off now could mean unlocking access to some of Chase’s most valuable welcome offers in just a short time.

Option 2: Shift Focus to Business Cards

You could also focus on business cards if you are eligible. That way you can keep earning bonuses and racking up points without jeopardizing your future Chase eligibility. Just make sure to stick to the listed banks above that don't typically report business cards on your personal credit card.

Option 3: Move On from Chase

If it will be a while before you're under 5/24 again, consider the opportunity cost of waiting. It might make more sense to continue pursuing valuable sign-up bonuses with other banks, rather than changing your strategy to get in Chase's good graces.

Final Thoughts

Chase issues some of the best rewards cards available in the U.S., including iconic travel credit cards like the Chase Sapphire Preferred® Card, Chase Sapphire Reserve®, and Ink Business Preferred® Credit Card. Understanding the 5/24 rule is essential if your rewards strategy includes Chase cards.

Getting back under 5/24 can require patience if you've recently opened too many accounts. But it can be worth the effort, assuming you calculate what you might miss out on while waiting to get back under 5/24. For anyone just starting out in the world of points and miles, planning your initial application strategy around the 5/24 rule will allow you to add Chase’s best rewards cards to your wallet before moving on to other card issuers.

$95Rates & Fees

- 5X points on Lyft rides through September 2027

- 5X points on travel purchased through Chase Travel℠

- 3X points on dining at restaurants worldwide

- 3X points on eligible streaming services

- 3X points on online grocery purchases (excluding Target, Walmart, and wholesale clubs)

- 2X points on all other travel

- 1X point per dollar spent on all other purchases

$795Rates & Fees

- 8x points on all purchases through Chase Travel℠

- 4x points on flights and hotels booked directly

- 3x points on dining worldwide

- 1x points on all other purchases

$95

- 3X points per $1 on the first $150,000 spent in combined purchases on travel, shipping purchases, Internet, cable and phone services, advertising purchases made with social media sites and search engines each account anniversary year

- 1X point per $1 on all other purchases

For rates and fees of the cards mentioned in this post, please visit the following links: Chase Sapphire Preferred® Card (Rates & Fees), and Chase Sapphire Reserve® (Rates & Fees)

![Understanding Rewards Credit Card Application Rules and Restrictions [2026]](https://awardwallet.com/blog/wp-content/uploads/2023/05/corinne-kutz-using-computer-featured.png)