AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

If your credit isn’t in pristine shape, you may be wondering what that means for your ability to collect points and miles toward travel with credit cards. A “fair” credit score does not mean you are shut out forever. It usually means you may see fewer card approvals, lower credit limits, or less favorable terms until your credit profile strengthens.

In this guide, we will define what a fair credit score really means, explain why scores get stuck there, and walk through the highest-impact steps to improve it.

What a Credit Score Measures

A credit score is a number that summarizes how risky you look to lenders based on what appears in your credit report. It reflects patterns such as whether you pay bills on time, how much of your available credit you use, and how long you have been using credit.

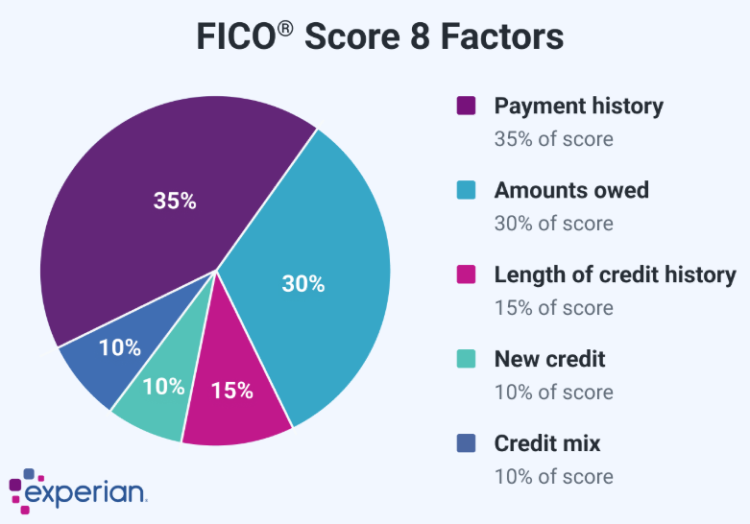

Most credit bureaus weigh a few factors more heavily than others:

- Payment history

- Credit usage

- Credit depth and length of history

- Recent credit activity

What a Fair Credit Score Means

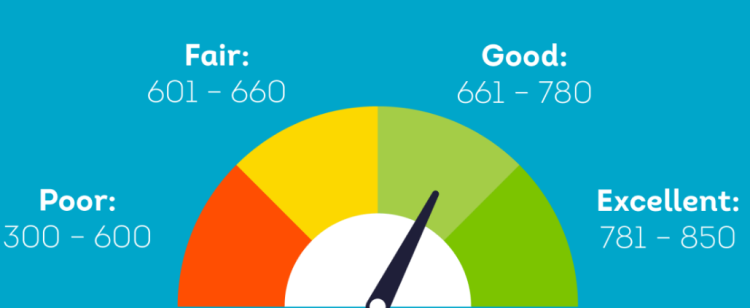

The three major credit bureaus — Equifax, Experian, and TransUnion — typically divide credit scores up into four categories: Poor, fair, good, and excellent/exceptional. Fair credit means your score is okay, but not strong, and it generally sits below what most systems label as good credit.

A fair credit score will usually fall in the range of the upper 500s to the mid-600s. The exact range can vary depending on the source and scoring model, and your score can also differ by bureau because not every lender reports to all three bureaus.

How can a fair score impact you?

Lenders generally view a fair credit score as moderate risk. It is not an automatic no, but it is not the type of score that reliably earns the best offers. In practical terms, a fair score often means:

- Higher interest rates

- Lower starting credit limits

- Tighter approval standards

- Fewer approvals for premium rewards cards

A fair credit score can make earning points and miles harder because it can limit which cards you qualify for and what terms you are offered. Most of the top cards that earn transferable points are marketed to applicants with good to excellent credit, so fair credit can mean fewer approvals, lower starting limits, and less attractive offers.

Why Your Credit Score Might Be Stuck in Fair

If your credit score is in the fair range, it is usually due to one of three things: utilization, late payments or other negative marks, or a thin or young credit file.

Utilization is simply how much of your available credit you are using at any given time, and it can weigh heavily on your score. If you have been extended $10,000 in credit and you have maxed that out, you have 100% utilization. Lenders consider credit utilization above 30% to be risky.

Late payments and derogatory items, like collections or charge-offs, can also keep a score from reaching the good range even if everything else looks fine.

The third common reason is that there just is not much history to score yet. If your accounts are new, you only have one or two accounts reporting, or you have not used credit consistently over time, your score may sit in the fair range because the system has limited data to evaluate.

How You Can Improve Your Fair Score

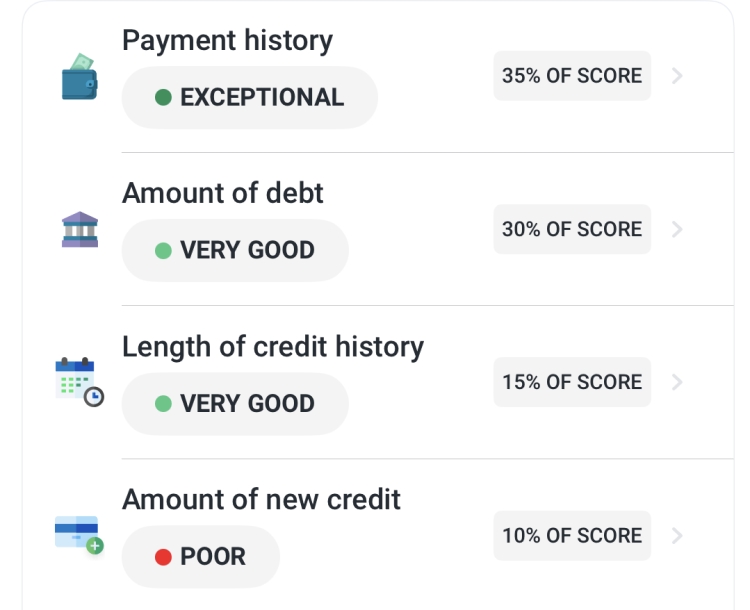

Before you start making changes, you need to know what is actually driving your score. A credit score is just the summary; your credit report is the source data. The fastest way to choose the right next steps is to review your reports from all three bureaus and look for the few items doing the most damage. You can pull your reports for free and scan for errors, past-due statuses, or accounts you do not recognize. Many free credit tools also flag the main score factors.

For example, I use the free Experian app, which highlights items like payment history, credit usage, length of credit history, new credit, and credit mix.

Here are some ways to increase your credit score:

Lower utilization

One of the quickest boosts to your credit score is to tackle your utilization. Credit utilization is simply how much of your available credit you are using. Because it is calculated using your balance relative to your credit limit, small changes in either number can move it quickly.

- Know your limits and keep balances low. A good rule of thumb is to avoid letting any single card report more than about 30% of its credit limit.

- Pay your balances in full. Paying the statement balance in full by the due date keeps you out of interest and prevents balances from piling up. If you are trying to manage utilization, it also helps to pay before the statement closes, since the statement balance is often what gets reported.

- Request a credit limit increase. Higher limits give you more breathing room and can lower your utilization without changing your spending. The key is to treat the extra limit as a cushion, not permission to spend more.

- Consider a new credit line. Opening a new card can increase your total available credit, which may help with utilization. (But do not apply for multiple cards at once, since frequent applications can work against you.)

If you have a trusted family member or close friend with strong credit, you can consider becoming an authorized user on one of their well-managed cards. This can be a simple way to add positive history to your credit profile. This works best when the primary cardholder has a long record of on-time payments and keeps balances low.

It can backfire if the account carries high balances, has any late payments, or if the primary cardholder is inconsistent. Before you do it, get clear on the basics: Will you receive and use a physical card? Or will you be added for credit-building only? How will spending be handled?

If becoming an authorized user is not an option, credit-builder products and secured cards can be the next-best route to improve your credit report.

Apply for a secured card

If your credit is fair because your credit history is limited or because you are rebuilding, the most straightforward path is to add positive payment history in a low-risk way. For many people, that means using a secured credit card designed specifically for establishing consistent, on-time payments.

A secured credit card is a starter credit card for building or rebuilding credit. It functions like a normal credit card, but you make a refundable security deposit up front. That deposit serves as the bank’s collateral and often determines your credit limit, which is why secured cards are usually easier to qualify for than unsecured rewards cards.

One example is the Capital One Platinum Secured Credit Card, which typically has no annual fee and no minimum credit score to qualify. Another credit-building option is the Secured Chime Credit Builder Visa® Credit Card, which is not a traditional secured card. Instead of borrowing against a credit limit, you use money you set aside to fund purchases, and your activity is reported to help build credit.

Use a credit-building service

A credit-building service is another way to improve your score by adding consistent, on-time payments to your credit report. These tools can be a practical option if you want a structured path to strengthening your credit profile.

Most credit-building services in this category work like an installment-style credit builder. When you make a fixed monthly payment, the service reports your payment history to the credit bureaus. As you stack on-time payments month after month, you build a stronger credit profile, especially if you have a limited credit history.

Two examples of installment-style credit builders are CreditStrong MAGNUM and the Self Credit Builder Account. Self also offers the option to add a secured card.

Mistakes That Can Slow Progress

Improving your credit score usually comes down to a few consistent habits, but it is surprisingly easy to undo your progress with the wrong moves. Here are the most common mistakes that slow people down, even when they are trying to do everything right:

- Closing old accounts: Closing a card can reduce your available credit and raise your utilization overnight. It can also shrink the overall age and depth of your credit profile over time. If the account has no annual fee and you are managing it responsibly, keeping it open is often the safer move. This is especially true if it is an account you've held for a long time.

- Lowering your credit limit: It can feel smart to reduce your available credit, like you are removing temptation. But lowering a credit limit often works against your score because it reduces your available credit and can push your utilization higher even if your spending does not change. A better approach is to keep the limit but put guardrails on your own behavior, like a smaller monthly budget or automatic payments, rather than shrinking your available credit.

- Carrying a balance: You do not need to carry a balance or pay interest to build credit. Scoring models reward on-time payments and responsible usage, not interest charges. Carrying a balance is simply an expensive habit that can make it harder to improve.

- Applying for too many cards at once: Multiple applications in a short window can create unnecessary noise on your credit report. Even if you get approved, opening several new accounts at once can lower the average age of your accounts and make you look riskier to lenders.

Bottom Line

A fair credit score is not a dead end. It is a signal that something specific in your credit report is holding you back. This is most often utilization, negative marks, or a limited credit history. The fastest way forward is to stop guessing. Base your next steps on what is actually showing up on your reports.

As your credit profile improves, so do your options for travel rewards. Better scores tend to unlock higher limits, stronger welcome offers, and the kind of rewards cards that make earning transferable points and miles much easier. Focus on the fundamentals, keep things consistent, and start qualifying for the cards that actually move your travel goals forward.