AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Well, the big day has finally come. Bilt Rewards’ new slate of credit cards officially launched on Wednesday. We’ve known for a while that this was coming, even as supposed leaks about card details were shot down by Bilt. The anticipation was as intense as anything we’ve seen in the credit card world since the re-launch of the Chase Sapphire Reserve® in mid-2025.

So now that the new cards are live, how did ardent fans and the broader internet respond? Let’s dig into the reactions.

Bilt Launches New Cards: How We Got Here

Let’s start with a brief history lesson. Bilt Rewards was founded in 2019 and launched in 2021 with a simple goal: To let renters earn rewards on their rent payments, which are often their largest monthly expense.

Throughout its short history, Bilt has delivered real value beyond points for rent payments. It offers one of the most robust lists of transfer partners in the loyalty world — including Hyatt, Alaska Airlines, and more. And its monthly Rent Day promotions can be extremely rewarding, especially for members with Bilt elite status. That combination has helped Bilt build a loyal following.

The “Bilt 1.0” credit card was a large part of Bilt's growth. However, it turns out that the card was a little too generous. The Wall Street Journal reported in 2024 that Wells Fargo was “losing as much as $10 million every month on the program.” Although Wells Fargo had the Bilt contract until 2029, Bilt and Wells Fargo announced the end of their partnership in mid-2025.

Bilt could clearly see the end of its lucrative card partnership coming and has been aggressively pivoting toward rewarding members who transact through Bilt’s network of merchants — known as “Bilt Neighborhood” — inking seemingly endless partnerships for earning and redeeming Bilt Points.

But Bilt didn't want to pivot completely away from the credit card space. After all, this is an environment where airlines often lose money on flying but make it back through lucrative credit card partnerships. This makes a strong card portfolio a potential kingmaker in today’s rewards landscape.

That brings us to the launch of Bilt's new credit card portfolio.

Internet and Media Reactions to the Launch of Bilt's New Cards

But despite all the good that Bilt Rewards has done over the past few years, the reaction to the launch of its new cards has been fierce.

Perhaps the biggest complaint: Earning Bilt Points on rent now requires either paying a transaction fee or redeeming Bilt Cash earned through card spend (Offer Terms).

Note: Bilt Cash expires at the end of each calendar year. Up to $100 of Bilt Cash earned rolls over to the next year.

To be clear, Bilt cardholders can still pay rent with no transaction fees. But you won't earn points and pay no transaction fees — as you could before. Instead, you'll either have to pay a transaction fee of 3% or redeem Bilt Cash to earn points on rent. And it's that new Bilt Cash program that's causing a lot of confusion and frustration.

Mainstream media

The New York Times dubbed the new program “the most complicated rewards system we've seen.” And it's hard not to agree with that.

The article raises real questions about how members will respond to Bilt’s new system of using Bilt Cash to offset rent and mortgage transaction fees. Under the new setup, in addition to earning Bilt Points, you'll earn 4% back on everyday purchases as Bilt Cash — a separate currency.

Once you’ve earned $30 in Bilt Cash, you can redeem it for 1,000 points (not Bilt Points, just points) that can be applied toward the 3% fee on your rent or mortgage payment. As Bilt explains, “If your rent is $2,000 and you have $60 of Bilt Cash, you can convert your Bilt Cash into 2,000 points on that payment, still with no transaction fee.”

It’s easy to see how this gets confusing.

The goal here is clearly to get cardholders to actually use their Bilt cards, not just swipe them 5 times a month (Bilt dubbed these cardholders the “Four Banana Club”) to earn free points on rent.

That makes sense from a business perspective. But for many longtime fans of the program, it also feels like a meaningful shift. And that’s where some of the pushback is coming from. A lot of it is already showing up on Reddit.

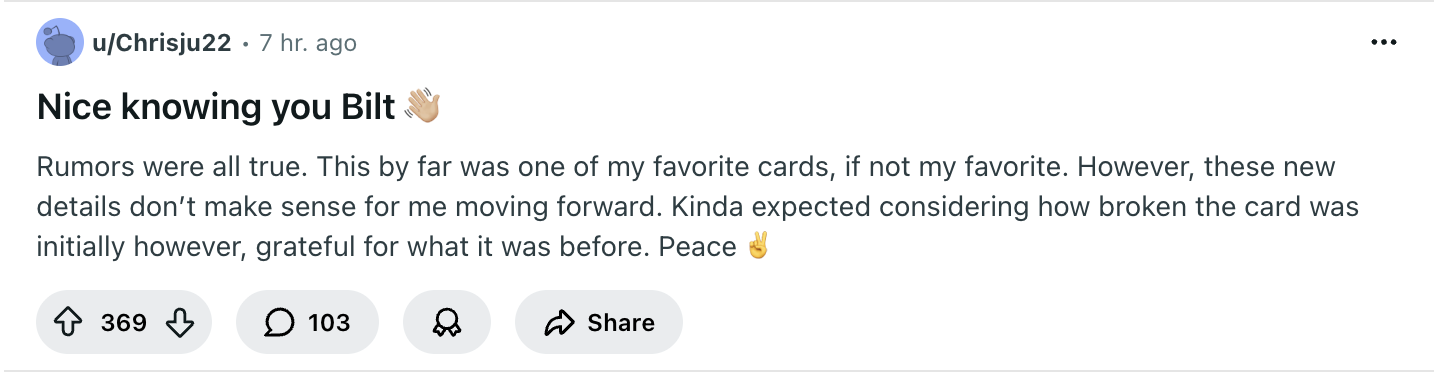

The “front page of the internet” has a dedicated community for Bilt fans at r/BiltRewards. It sees about 81,000 weekly visitors. There, the response has been largely negative.

Even when the reaction hasn’t been outright negative, the conversation has exploded in popularity. The most popular thread has topped 444 comments, and much of the discussion echoes the concerns raised in The New York Times. People are trying to understand the new system but are running into confusion about how it all works. To his credit, Bilt’s GM of Travel, Richard Kerr, even hosted an AMA to answer questions.

Others are disappointed that some of the strongest benefits from the no-fee card have shifted to the $95 annual fee card. One user, “quackjacks,” summed it up well:

“I use my Bilt card as a daily driver and spend quite a bit, but if I’m reading this correctly, I have to pay a $95 annual fee to keep the 3x dining and 2x travel that I used to get without an annual fee. What’s the upside?”

Fair point.

Bottom Line

I expected the initial response to be negative because the “gravy train,” of sorts, is ending for certain Bilt members. But I think we need some time to fully assess the new program. Bilt Cash can also be used for purchases within the Bilt ecosystem, but the program hasn’t yet defined the full limits on how much you can redeem each month. There could be real value there, on top of earning Bilt Points.

For me personally, as a homeowner, I’m still deciding whether the Bilt Palladium Card (Rates & Fees) deserves a spot in my wallet. The idea of finally being able to participate in the lucrative Rent Day promotions — assuming they continue in their past form — is very enticing. But the card fee isn't minimal.

- Earn points on housing payments with no transaction fee

- Choose to earn 4% back in Bilt Cash on everyday spend. Use Bilt Cash to unlock point earnings on rent and mortgage payments with no transaction fee, up to 1X.

- 2X points on everyday spend

- $400 Bilt Travel Hotel credit. Applied twice a year, as $200 statement credits, for qualifying Bilt Travel Portal hotel bookings.

- $200 Bilt Cash (awarded annually). At the end of each calendar year, any Bilt Cash balance over $100 will expire.

- Welcome bonus (subject to approval): 50,000 Bilt Points + Gold Status after spending $4,000 on everyday purchases in the first 90 days + $300 of Bilt Cash.

- Priority Pass ($469/year value). See Guide to Benefits.

- Bilt Point redemptions include airlines, hotels, future rent and mortgage payments, Lyft rides, statement credits, student loan balances, a down payment on a home, and more.

- Choose to earn 4% back in Bilt Cash on everyday spend. Use Bilt Cash to unlock point earnings on rent and mortgage payments with no transaction fee, up to 1X.

- 2X points on everyday spend

What's your reaction to the new Bilt cards?

For rates and fees of the cards mentioned in this post, please visit the following links: Bilt Palladium Card (Rates & Fees)