![[Expired] Chase Automatically Extending Sign-Up Bonus Spending Period for Some Cardholders](https://awardwallet.com/blog/wp-content/uploads/2020/04/AdobeStock_286492496-1024x288.jpeg)

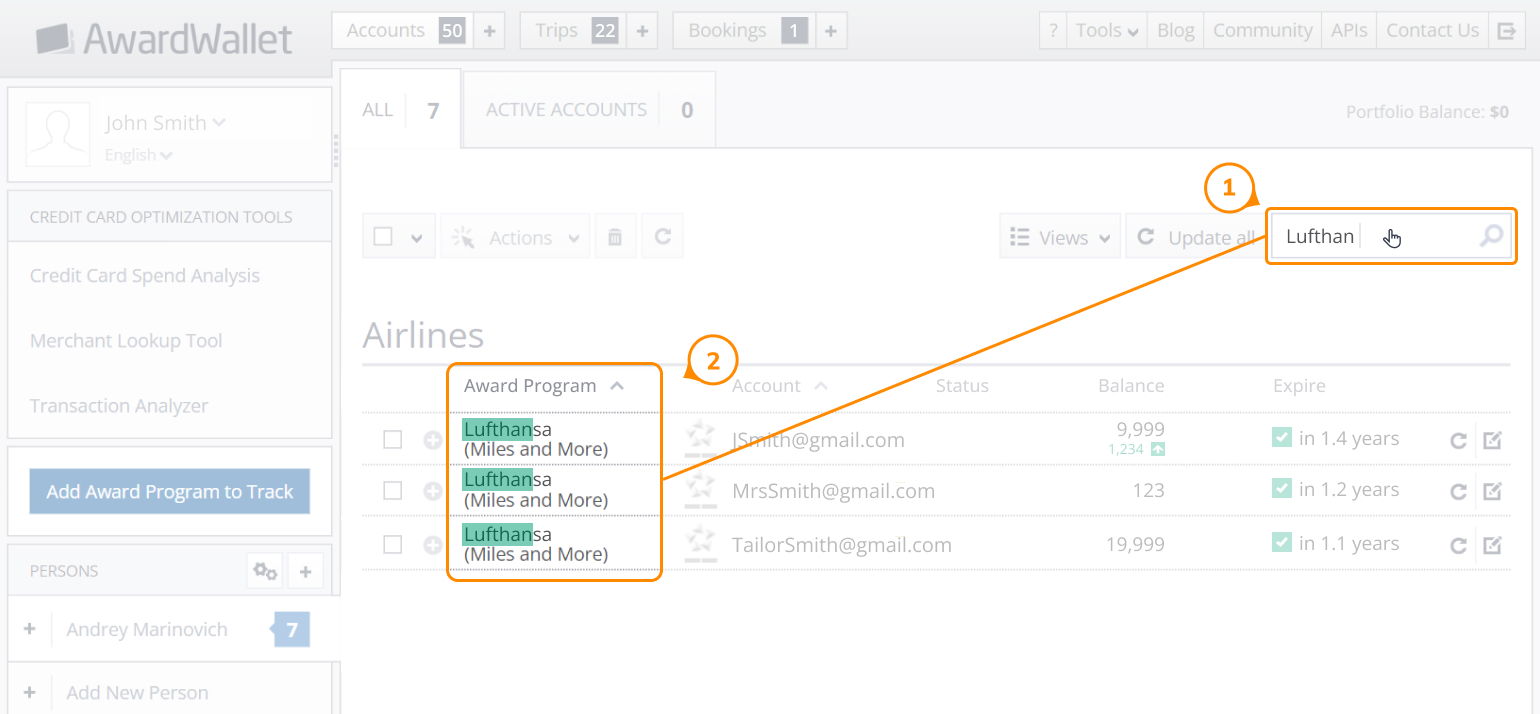

![[Expired] Chase Automatically Extending Sign-Up Bonus Spending Period for Some Cardholders](https://awardwallet.com/blog/wp-content/uploads/2020/04/chase-bank-feature-e1587084426387.jpg)

AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

This promotion has ended; please review current/active promotions.

There isn't a lot of great news in the travel world these days but Chase has some for new cardholders. Following the lead of American Express, Chase is extending the deadline to meet the spending requirements for many sign-up bonuses.

Sign-up Bonus Extension

Whether you were eyeing the signup bonus on the Chase Sapphire Reserve® or the Ink Business Preferred® Credit Card, no one wants to miss out on earning valuable sign-up bonuses because travel and spending routines have been disrupted.

Thankfully, Chase cardholders who applied for new accounts between January 1, 2020, and March 31, 2020, now have more time to meet their spending requirements. As originally reported by Miles to Memories and confirmed by AwardWallet, the spending requirement deadline will automatically be extended by three months. That's great news for new cardholders whose travel and spending patterns have changed because of COVID-19.

Our Take

While the three-month extension is great news for new cardholders, we haven't seen all the details in writing from Chase just yet. Cardholders who opened accounts between January 1 and March 31, 2020 should check their emails and account pages for specific updates.

Given that travel and spending patterns don't seem like they will be back to normal quickly, we will keep looking for a public announcement. It's certainly possible that Chase is still fine-tuning its policies and will have more details coming soon!

The comments on this page are not provided, reviewed, or otherwise approved by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.