AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

To unlock the benefits of travel rewards credit cards and maximize their perks, you need to maintain an excellent credit score. In addition to valuable points and miles that can be redeemed for travel, card benefits include airport lounge access, travel insurance, and free or discounted companion airfares.

Even if you don't need or want to open a ton of credit cards, managing your credit score is still important in other aspects of life, such as renting or buying a home, purchasing a car, or applying for a loan. There's a lot to know about managing your credit score, including best practices to keep your score high. Here are our best tips to help you do just that.

Page Contents

The Importance of Managing Your Credit Score

The importance of maintaining an excellent credit score cannot be overstated, especially when it comes to using credit cards to earn points and miles. The best credit card sign-up bonuses are typically reserved for those with great to excellent credit scores.

The first step in managing your credit score is understanding where you currently stand by getting a snapshot of your current score. From there, we'll help you learn what goes into calculating your credit score to figure out what you can do to improve or maintain it.

Related: A Beginner's Guide to Building Healthy Credit

How To Check Your Credit Score Online

There are several ways to check your credit score for free. Here's an overview of a few of the options you have.

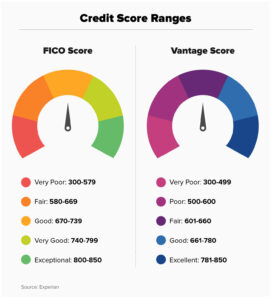

MyFICO

One popular way to check your credit score online is through myFICO, which provides you with your official FICO score from up to three credit bureaus. This is the same service that roughly 90% of lenders in the U.S. use to determine your creditworthiness. It's the easiest way to see the same data that lenders will be using to assess your credit card applications. If you'd like to see your FICO score from all three credit bureaus, you will need to sign up for a membership starting at $19.95 per month.

However, the free version of myFICO is also an option to receive a monthly report that includes your FICO score and credit report from Equifax. This version also includes credit monitoring and is an excellent option for getting a regular snapshot of your credit score.

Credit Sesame or Credit Karma

Companies like Credit Sesame or Credit Karma are completely free and allow you to retrieve your credit info. They also offer a wealth of information about what is affecting your credit score. Additionally, they provide tips and tricks to help raise your score.

Credit Sesame and Credit Karma don't provide your FICO score, but rather your credit score based on the VantageScore model, an alternate credit scoring model based on all three credit bureaus. The FICO score is specific to each bureau.

We recommend signing up for a service like the ones mentioned above to see a broader picture of your financial situation than what you'd get from your credit report alone.

Options available through your bank

Most banks provide you with free credit services as well if you have a credit or checking account. A good example of this is Chase Credit Journey, which is available to Chase bank account holders and credit cardholders.

Your best bet is to monitor your credit through multiple sources or all of the sources listed here. That way, you can see the possible variations in your credit score or report that might be affecting your creditworthiness.

One helpful note: When getting ready to apply for a new credit card, check your score with the bank you're applying with if you already have another account with them. This ensures that you see precisely what the bank is taking into consideration for your application.

How Credit Scores Are Calculated

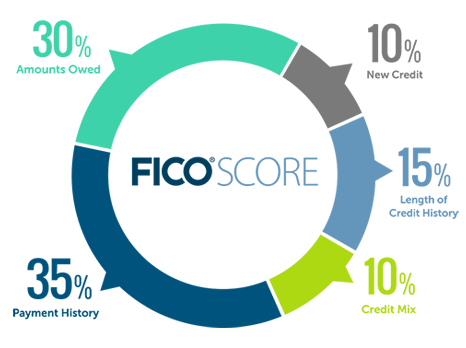

Credit scores are complex. They're compiled using your lending history and financial data. If your credit score isn't where you want it to be, the first step to improving it is to understand what factors go into your score in the first place.

Here are the factors that are taken into account when determining your credit score:

- Payment history (35%): Lenders are looking for “on time, every time” customers. Late payments represent a higher risk, and anything over 30 days will start to impact your credit score.

- Amounts owed (30%): This number is not calculated on the raw sum of money owed. Instead, it's calculated based on your utilization rate, or the proportion of available credit compared to how much is being used. Lenders are looking for utilization rates under 30%, which will earn you a better credit score.

- Note: The impact of these inquiries starts to fade immediately. Over one year, those dips from inquiries will disappear.

Tips to Manage Your Credit Score

Always pay your account on time

The single most important factor in managing your credit score is paying your accounts on time. Never let your payments fall behind. You can even set up automatic payments each month or alerts to remind you to pay your credit card.

In addition, personal finance software, like Monarch or You Need A Budget, helps you to keep track of what's due (as well as other financial and budgeting organizing).

Keep credit utilization under 30%

Under 30% is good, but under 10% is even better. Studies have shown that keeping credit utilization ratios under 10% gives you the best possible chance of achieving an 800+ score (considered “exceptional”). It's also worth noting that keeping the balances on your credit cards low can potentially save you thousands in interest over the lifetime of an account.

Downgrade rather than close or cancel accounts

Closing accounts can have a negative impact in two ways. First, you might have less available credit, which can increase your credit utilization ratio. Second, it can affect the average age of your accounts, especially if you close one of your older accounts. We recommend always keeping your oldest card open, even if you never use it. Rather than canceling a credit card, look at downgrade options from the same provider.

Related: You Shouldn’t Cancel a Credit Card Within Your First Year of Membership. Here’s Why.

Set regular times to assess your credit score

One of the worst things you can do for your credit score is to ignore it. Setting bi-monthly or quarterly dates to monitor and assess your credit score will help you manage it and make plans to raise it, should that be necessary. You can stay on top of things that may be negatively impacting your score by catching them early during these check-ins. It’s also an excellent way to prevent fraud.

How to Fix Bad Credit

Fixing a bad or less-than-ideal credit score takes time to fix. Luckily, however, there are a few tips to help fix a credit score that needs a little TLC.

Make on-time payments

Even if it's just the minimum payment on a card that you can't pay in full each month, paying on your due date is very important. On-time payments and payment history are the most significant factors that credit bureaus take into consideration when calculating your credit score.

Lower your credit card utilization ratio

You can lower your credit card utilization ratio in one of two ways. For the sake of paying less in interest that accumulates from carrying a balance each month, you can pay down your credit cards. Or, you can request a credit increase on the cards you already have. By increasing the credit available to you, the bureaus see you as having more credit than you have debt.

However, just be aware that requesting a credit limit increase typically results in an inquiry, or hard pull, on your credit, which is something to keep in mind.

Be patient

Paying off debt can make your credit score jump a few points, but building creditworthiness takes time. Credit bureaus like to see consistent on-time payments and a longer credit history, meaning accounts that have been open and in good standing for a while. The only way to have either of these things is time.

Final Thoughts

Correctly tracking and managing your credit score is one of the most important factors in successful rewards travel planning. It gives you the highest possible chance of being approved for the best credit cards with the best perks. It also gives you the lowest interest rates, potentially saving you thousands of dollars in interest over the life of each credit account.

We highly recommend that your first step be to set up an account with a service like myFICO or Credit Karma to monitor your credit scores and create a plan to get your score as high as possible. You’ll find a good credit plan gives you the best possible chance of success when taking on rewards travel as a hobby.