AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Your credit is as critical to your financial health as any physical asset you might own. Healthy credit makes borrowing easier, helps you qualify for the best rewards credit cards, and unlocks preferential interest rates on major purchases like homes and cars. Simply put, having healthy credit is more important than you may realize.

One common misconception is that opening new credit cards or maximizing rewards will hurt your credit score. This isn’t true. In this guide, we’ll break down how credit scores are calculated and provide actionable tips to build and maintain healthy credit.

Page Contents

- Why You Need Healthy Credit to Earn Credit Card Rewards

- 5 Quick Tips to Build Healthy Credit

- Understanding Credit Scores and Reporting

- How Your Credit Score is Calculated

- How Does Opening Credit Cards Affect My Credit Score?

- How Does Closing Credit Cards Affect My Credit Score?

- Avoid Negative Impacts When Closing a Credit Card

- Final Thoughts

Why You Need Healthy Credit to Earn Credit Card Rewards

In recent years, banks in the United States have become central players in the travel and credit card rewards ecosystem. These institutions spend billions annually to purchase points and miles from airlines and hotels to attract credit card customers and fund rewards programs that have become household names.

For those who live in the U.S., many of the best opportunities to earn rewards, whether in points, miles, or cashback, are directly tied to credit cards. With healthy credit, you can qualify for the best rewards cards that offer lucrative sign-up bonuses, valuable long-term perks, and generous rewards for everyday purchases.

Over time, these rewards can translate into free (or nearly free) travel or extra cash in your bank account. But without healthy credit, you're unlikely to qualify for many of the best cards.

5 Quick Tips to Build Healthy Credit

There are plenty of strategies to build and maintain healthy credit. But if you're looking for the highlights, put these five tips into practice:

- Pay on time, every time. Payment history is the most important factor in your credit score. Setting up automatic payments for at least the minimum amount ensures you’ll never miss a due date.

- Keep credit utilization below 30%. Aim to use less than 30% of your available credit to avoid appearing overextended. Lower utilization (under 10%) can further boost your score.

- Don’t close your oldest accounts. Older accounts contribute to your credit history. If possible, keep your oldest card open, even if it’s just a no-annual-fee account.

- Space out your credit applications. Too many hard inquiries in a short period can temporarily lower your score. Apply for new cards strategically.

- Maintain a diverse credit mix. Lenders favor borrowers with a mix of credit types (e.g., credit cards, auto loans, mortgages). Diversifying your credit portfolio shows you can manage different types of debt responsibly.

Related: Tips for Managing Your Credit Score

Understanding Credit Scores and Reporting

Credit bureaus

Credit bureaus are companies that track your credit history and compile reports that lenders use to evaluate your creditworthiness. The three major bureaus are:

Each bureau collects data independently, so your credit reports may vary depending on which one you check. And mistakes can happen, so it’s wise to monitor your credit regularly. Free credit monitoring services can provide much of the same information as paid subscriptions.

Related: How To Check Your Credit Score for Free

Credit scoring models

The most widely used credit score is FICO®, created by the Fair Isaac Corporation. FICO scores range from 300 to 850, with higher scores indicating lower risk to lenders. Many banks offer free access to your FICO score, often as a benefit tied to your credit card.

Another popular scoring model is VantageScore, developed by the three bureaus. It uses the same 300–850 range but weighs factors differently.

Both models evaluate your credit using a handful of key factors, which we’ll cover in detail below.

One of the easiest ways to keep track of your credit score is through AwardWallet. Just link a bank program that offer free credit scores — such as American Express or Barclays — and AwardWallet will retrieve these when updating your account. AwardWallet Plus members can even view a chart of how their score changed over time.

How Your Credit Score is Calculated

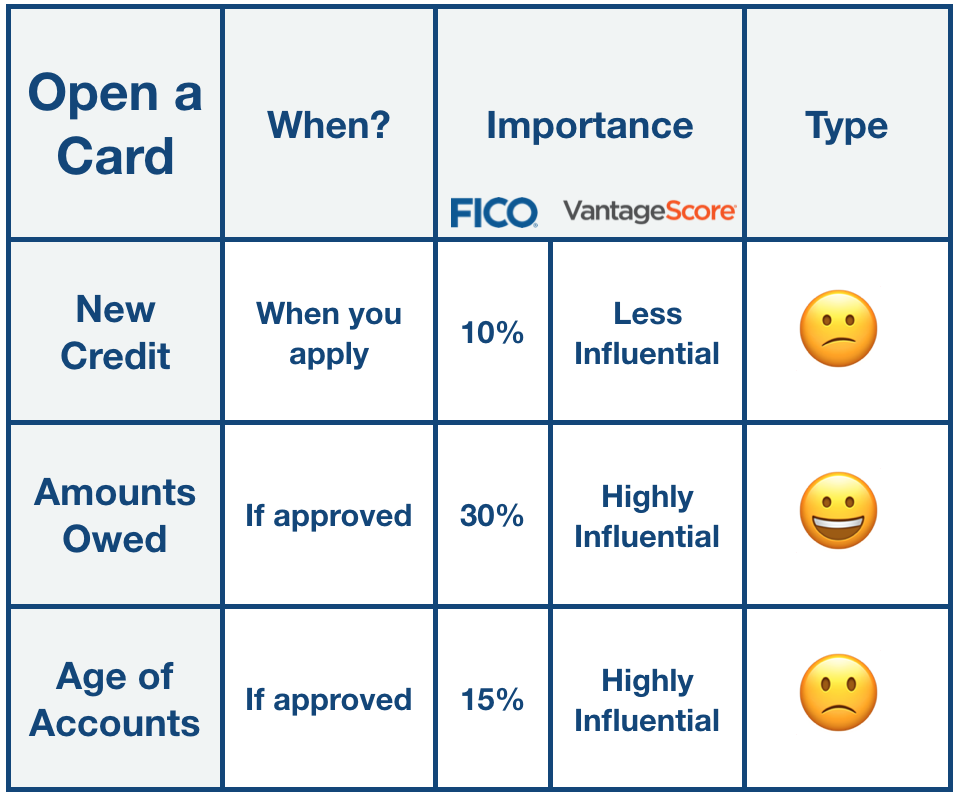

FICO and VantageScore use the same five factors to calculate your credit score, although each weighs these factors differently. FICO gives percentages for how much weight is associated with each factor. VantageScore assigns relative importance instead. Understanding which factors are most important can help you focus on those as you build healthy credit.

| Credit Factors | FICO | VantageScore |

|---|---|---|

| Payment History | 35% | Extremely Influential |

| Amounts Owed | 30% | Highly Influential |

| Age of Accounts | 15% | Highly Influential |

| New Credit | 10% | Less Influential |

| Credit Mix | 10% | Moderately Influential |

Payment history

Lenders want customers who pay their bills on time. This factor only considers whether you made the minimum payments each month. We recommend going beyond that, though. If you don't pay your full credit card balance each month, you will pay interest, which is expensive and eats up the value of your rewards.

Related: The Best Rewards Credit Cards Featuring 0% APR on Purchases

If you make a late payment, don't panic. Anything less than 30 days late shouldn't affect your score (the banks will likely not report this to credit agencies). But don't make a habit of it. A best practice is to set up automatic payments covering at least the minimum payment.

Amounts owed (credit utilization)

Your credit utilization is the amount of your available credit that you are currently using. If you have one credit card with a credit limit of $10,000 and a monthly statement balance of $5,000, then your credit utilization is 50% ($5,000 / $10,000).

Use less than 30% of your available credit whenever possible, but using less than 10% is even better. Your credit score will consider your total utilization across all accounts and on each individual account. That means a 10% utilization on one card and a 95% utilization on another card can still hurt you.

It's worth noting that your amounts owed (and credit limits) are reported to the credit bureaus each month — typically when your statement closes. Even if you pay off your full statement balance on the due date, your credit report will reflect the utilization rate at the end of your billing cycle. Making a partial payment before your statement closes will lower your credit utilization at statement closing. Then, the credit bureaus will see a lower utilization rate.

Related: Buy Now, Pay Later Programs — And Why You Should Skip Them

Age of accounts (length of credit history)

Your average age of accounts considers your oldest account, newest account, and an unweighted average age for all accounts on your credit report. The exact formula isn't known. Conventional wisdom, though, is that your oldest accounts (and especially the oldest account) are most important for this metric. This metric makes up 15% of your FICO score and is rated as “highly influential” with VantageScore.

Older accounts with a long history of on-time payments and responsible credit utilization give lenders better insight into your behavior over time. A brand-new account isn't likely to predict future risk, but a seven-year-old account should inspire more confidence. Thus, it's important to keep old accounts open and in good standing. If you have an old card that you don't use much, it's a good idea to use it at least twice a year so the bank won't close it. That would likely bring down your average age of accounts.

New credit

When you apply for a loan or credit card, the lender requests a copy of your credit report from one or more of the three credit bureaus. This credit check (also known as an “inquiry” or “hard pull”) is added to your report for two years.

With each inquiry, your credit score will decrease a small amount — typically around five points. The effect can be greater when multiple new credit inquiries are added in quick succession, particularly if you don’t have a long credit history. Fortunately, new credit is a small part of your overall score, and the impact of credit inquiries starts to fade almost immediately. It's also offset by other factors that carry more weight.

Credit mix

This factor considers your entire lending mix, including credit cards, personal loans, finance accounts, mortgages, and external factors, such as being a guarantor or authorized user on another account.

Related: Does Being an Authorized User Affect Your Credit?

Lenders like to see that you can manage multiple types of credit. If you can manage a mortgage, car payment, and multiple credit cards (known as revolving accounts), you look less risky to a mortgage lender than someone with only credit card accounts on their credit report.

How Does Opening Credit Cards Affect My Credit Score?

Many people assume that opening a new credit card will hurt their credit score and avoid cards while trying to build healthy credit. In the short run, this can be true, due to the new inquiry and likely decreasing your average age of accounts. However, both positive and negative factors are at play. If the positive outweighs the negative, you may see a significant increase in your score after opening a new credit card account.

Let's look at how applying for a new credit card can affect these factors:

Negative impact: New credit

When you apply for a card, the bank will pull your credit report from one (or more) credit bureau. This falls into the “New Credit” category, composing 10% of your FICO score and “less influential” for VantageScore. This factor takes effect when you apply for the card — regardless of whether you get approved.

A hard inquiry will stay on your credit report for two years, but its effects decrease over time. According to Experian, new inquiries typically stop hurting your credit report after a few months.

Negative impact: Age of accounts

When you open a new card, the average age of the accounts on your credit report is reduced. However, the degree to which this affects your score depends on the rest of your credit history. If you have lots of other accounts with a long history, a new credit card may barely change your average age of accounts. On the other hand, if this is only your second credit card, the new account could cut your average age in half.

This factor accounts for 15% of your FICO score and is rated as “highly influential” by VantageScore — more important than the “new credit” category — and the impact will last longer, though it's a relatively small part of your overall credit score.

Positive impact: Credit utilization

Credit utilization is the percentage of your available credit you're using. When you're approved for a new card, you'll get a new line of credit. If your spending stays constant, the additional credit reduces your utilization and should improve your score.

As with the age of accounts, the magnitude of this impact depends on the rest of your credit file. A person with lots of available credit won't see a big change in utilization.

Utilization is twice as important to your FICO score as your average age of accounts, which is why many people see their credit improve after opening a new card. VantageScore considers both “highly influential,” but it's still possible that this positive factor will outweigh the negatives.

Credit utilization is a big reason opening cards (and keeping them open over time) can increase your credit score. The more available credit you have, the lower your utilization — assuming your spending doesn't go up. Low utilization makes you look less risky, which is what a credit score is trying to determine.

Positive impact: Credit mix

There is one additional factor that might come into play. Credit mix makes up 10% of your FICO score and is rated “less influential” by VantageScore. If you don't already have other credit cards, opening a new one can add to the diversity of your credit portfolio. Your first or second credit card may have a modest, positive impact on this factor.

Related: Understanding Credit Card Application Rules and Restrictions

How Does Closing Credit Cards Affect My Credit Score?

There are many valid reasons to close a credit card, such as not wanting to pay the annual fee or simplifying your wallet. Most of the credit impacts from closing a credit card are negative — though they're minor, thankfully.

Negative impact: Credit utilization

Closing a card usually means giving up your line of credit. If the account you close makes up a small percentage of your total available credit, the impact on your utilization should be relatively small. However, this can be a major factor if you don't have other significant lines of credit or are closing a card with a large credit line.

We'll discuss how to negate this below.

Negative impact: Length of credit history

Closed accounts don’t get any older, so this card won't mature and help your average account age. If you close one of your older accounts, you may significantly reduce the average age of the accounts on your credit report. However, the timing of this impact depends on the credit scoring model used to generate a credit score.

Closed accounts (along with their payment history) stay on your history for 7–10 years after closure. The FICO score considers the age of both open and closed accounts for as long as they remain on your credit report. That means your length of credit history won't be affected immediately when closing a card.

VantageScore doesn't provide definitive information on how closed accounts factor into your score. Most sources say that VantageScore considers closed accounts when calculating your age of accounts.

When the account drops off eventually, you may see a small score impact, due to a change in your average age of accounts. However, this won't drastically affect your efforts to build healthy credit and a good credit score.

Avoid Negative Impacts When Closing a Credit Card

It's possible to limit the negative effects of closing a card. One option is to consider downgrading to a no-annual-fee card to preserve the age of the account and credit limit. When you downgrade a card (also known as a product change), the account history is normally preserved. Your bank may mail you a new card — and hopefully, refund that annual fee — but the credit bureaus will usually treat the converted account as a continuation of the old one.

It's worth noting that this doesn't always work. As a general rule, your age of account won't be affected if you keep the same credit card number through the transition. If your bank says your account number will change when you downgrade your card, the credit bureaus may treat this as a new account with respect to your age of accounts. Be sure to ask your bank during the product change process.

If you decide to close an account, you may be able to move your line of credit to another account with the same bank. This preserves your total available credit. If your spending stays constant, closing that card won't hurt your overall credit utilization.

Final Thoughts

Learning and reading about how to build healthy credit isn't fun, but it's essential for maximizing your opportunities with points and miles. Healthy credit will open the door to the best rewards cards — offering lucrative sign-up bonuses and access to benefits that make travel more enjoyable.

Even if you take a casual approach to points and miles — or don't participate at all — healthy credit is important. It provides access to the best interest rates when purchasing a home or car. This can provide thousands of dollars in savings over your lifetime.

This is an article that many people should read. I have approximately 20 cards and almost a maximum credit score. I have no other debt and I’m not going to take any on just to improve it.

I actually didn’t realize that different types of credit were important, but once your score is over 800, it probably doesn’t matter.

Really helpful article! I was planning to close one of my cards, mainly because I was not using it. But thanks to this post I learnt it is better to downgrade to a no-fee card. And with this I preserved my credit limit, something I was going to lose without realizing if I had not read this article. MANY THANKS!!

I enjoyed reading this article, it’s been quite informative. My husband is a points and miles fan, and he got me started on my credit “journey” with the Capital One Quicksilver. It’s nice to earn something back for purchases I was making all the time anyway with debit and cash. I’ll be sure to refer back to this article from time to time for a refresher on how to maximize my credit score. Thanks!

Once I started paying off my credit card balance just about every day, my credit score really took off – avoiding a balance where possible when my statement closed really helped bump up my score.

It’s not just cards that are considered when calculating the age of your oldest account. I found that out the hard way when I paid off my first student loan; I thought I would see my credit go up a bit since I paid off a large loan, but instead it dipped for about 6 months because it registered as a closed account.

In addition, some employers check your credit history to find out how “responsible” you have been handling your finances in the past, in an effort to judge whether you are a good candidate

I noticed that my score has dropped more than expected after opening a couple of new cards recently. Now I see that it’s probably because of the average age of accounts going down! I did not realize that category was highly influential. Is there a target credit score that one should be careful to stay above to be able to be approved for the best credit cards?

It depends on the bank/card issuer, the particular card, and even the economy! But, a credit score of over 700 is generally best for the best rewards cards. The good news is that you’ll recover most of the credit score hit in the next couple of months.

How would the credit score be affected if one maxes out the credit allowance frequently but always pays the balance in full?

Nice breakdown, especially for those stumbling into this “game” and those who need a refresher.

Found this article very helpful, thanks

Useful article, young adults should be taught this.

Interesting article, very detailed and easy to read.