AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

If you’re new to points and miles, it’s easy to feel overwhelmed. There’s no shortage of advice out there — especially when it comes to credit cards. So today, we’re going back to the basics with a look at one of the best beginner travel rewards cards on the market: the Chase Sapphire Preferred® Card (Rates & Fees).

We’re breaking it down using seven key factors that matter when picking your first travel credit card. Along the way, you’ll see why the Sapphire Preferred is a top choice for beginners — even after you earn the incredible welcome bonus.

- Earn 100,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening.

- Enjoy benefits such as 5x on travel purchased through Chase Travel℠, 3x on dining, 3x on vacation homes, 3x on gas & EV charging, 3x on top streaming services and online groceries (excluding Walmart, Target, and wholesale clubs), 2x on all other travel purchases, 1x on all other purchases

- Earn up to $100 in statement credits each account anniversary year for hotel stays through Chase Travel

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Collision Damage Waiver, Lost Luggage Insurance and more.

- Get a year of complimentary Apple TV when activated by December 31, 2026 - a value of $156.

- Complimentary DashPass which unlocks $0 delivery fees & lower service fees for a min. of one year when you activate by 12/31/27. Plus, a $10 promo each month on non-restaurant orders.

- Receive one statement credit of up to $120 every four years as reimbursement for the application fee charged to your card for a Global Entry, TSA Precheck® or NEXUS application.

- Transfer points to leading airline and hotel loyalty programs

- Member FDIC

- 5X points on Lyft rides through September 2027

- 5X points on travel purchased through Chase Travel℠

- 3X points on dining at restaurants worldwide

- 3X points on gas and EV charging

- 3X points on vacation homes at top brands like Airbnb, Vrbo and more

- 3X points on eligible streaming services

- 3X points on online grocery purchases (excluding Target, Walmart, and wholesale clubs)

- 2X points on all other travel

- 1X point per dollar spent on all other purchases

Page Contents

What Makes a Great Beginner's Credit Card?

We think seven factors make a card stand out for beginners:

- A valuable welcome bonus for new cardmembers

- A reasonable spending requirement to earn the bonus

- Easy ways to redeem points (without needing a PhD)

- The potential to redeem points for maximum value

- Points that are easy to earn on everyday purchases

- A low annual fee

- Solid additional cardmember benefits

Let’s look at how the Sapphire Preferred checks all those boxes.

Receive a Valuable Welcome Offer

Credit card issuers make a lot of money on cardholder spending — and welcome bonuses are how they get your attention in the first place. A generous bonus is their way of getting you to choose its card over someone else’s.

A typical credit card sign-up bonus has three aspects. The signup bonus (the number of points you can earn), a spending requirement (what it takes to earn the reward), and a time period for you to earn it.

Right now, the Sapphire Preferred is offering a whopping 100,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening. But it's ending very soon, so if you think this is the card for you, run, don't walk.

Welcome offers for the Sapphire Preferred range between 50,000 and 100,000 Ultimate Rewards.

Iberia business class. Credit: Ben Nickel-D'AndreaWhen comparing credit cards, it’s important to remember that not all points are created equal. A 100,000-point bonus from one program might be worth far more (or far less) than the same number of points in another.

Stick with us to learn some of the reasons why Chase Ultimate Rewards are one of the most valuable rewards currencies available.

Meet a Reasonable Spending Requirement

Earning a welcome bonus is usually an all-or-nothing deal. If you don’t hit the spending requirement in time, you won’t earn any of the bonus points. There is no sliding scale. And while it’s tempting to spend more than you normally would just to hit the threshold, the ideal approach is to move spending you already make onto your new card.

What counts as a “reasonable” spending requirement depends on your own monthly budget. However, several strategies can help you meet the spending requirement without going overboard. Here are some quick examples:

- Pay your monthly bills — Things like power, internet, phone, insurance, daycare, auto maintenance, and even pet care can add up quickly and contribute to your minimum spend.

- Pay your taxes with a credit card — If you time your application well or make estimated quarterly payments, you could meet the entire spending requirement in one go. Services like Pay1040 or ACI Payments, Inc. let you pay for a ~1.75% fee. It's not a great deal if you're earning just one point per dollar, but more justifiable if you’re unlocking a large signup bonus.

- Pay by check with a credit card — Plastiq lets you send a check using your credit card. It’s useful for large expenses like rent or college tuition. Just be aware of the 2.90% service fee.

- Front-load your expenses — Many providers allow prepayment. For example, when we got a $150 utility bill, we paid $450, creating a credit on the account. We’ve also prepaid our HOA fees and property taxes — all to help hit a minimum spend threshold.

Redeem Points Without an Advanced Degree

One of the most frustrating things about rewards programs is how complicated they can be. Some programs are so complex that you practically need a PhD to use your points effectively. That’s where the Chase Ultimate Rewards program shines as one of the best beginner travel credit cards.

At a minimum, you can redeem points for statement credit at 1 cent per point. That should be your baseline value.

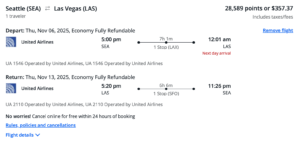

You can boost that redemption rate and get up to 1.5 cents per point (depending on your specific redemption) just by using them to book travel through the Chase Travel℠ portal. Doing so is incredibly easy. For example, I was able to redeem 25,589 points for flights from Seattle to Las Vegas round trip for a value of $357.37.

Even better, booking hotels through the Chase portal can trigger the card’s $100 annual hotel credit, which helps offset the card’s annual fee.

Related: Do Chase Points Expire?

Enjoy Ways to Redeem Points for Maximum Value

You won't be a beginner forever if you stick with us. So, it's important to earn points that have a higher upside as you gain more experience with redemption strategies.

In addition, having a card that earns flexible, transferable points is one of the best moves you can make — whether you’re a beginner or a seasoned expert. You’re not locked into a single airline or hotel program. You can keep your options open and choose the best redemption when the time is right.

Chase Ultimate Rewards are special because they can be transferred at a 1:1 ratio to 14 partner loyalty programs. These transfer partners often require far fewer points than you'd pay by booking through the Chase travel portal, creating the opportunity to unlock outsize value.

Ultimate Rewards points transfer into World of Hyatt at a 4:3 rate for the Sapphire Preferred, and because most Hyatt hotels are priced in category bands, you can redeem a set number of points for some top-notch hotels. For example, I transferred my points so I could book a one-week stay at the Palacio Duhau – Park Hyatt Buenos Aires that would have cost me a few thousand dollars otherwise.

Collect Points That are Easy to Earn

Another reason the Sapphire Preferred stands out is how easy it is to rack up points from everyday spending:

- 5X points on Lyft rides through September 2027

- 5X points on travel purchased through Chase Travel℠

- 3X points on dining at restaurants worldwide

- 3X points on gas and EV charging

- 3X points on vacation homes at top brands like Airbnb, Vrbo and more

- 3X points on eligible streaming services

- 3X points on online grocery purchases (excluding Target, Walmart, and wholesale clubs)

- 2X points on all other travel

- 1X point per dollar spent on all other purchases

This card also has no foreign transaction fees, making it a reliable option when traveling internationally.

Earn more points by creating a card pairing

If you want to fast-track accumulating points earned, you can combine points from multiple Ultimate Rewards earning cards into a single account. We've written a comprehensive post about how to put together the ultimate Chase travel rewards card combo.

This lets you earn a ton of bonus points across different spending categories since virtually all of your purchases could fall into one of the multiple cards' bonus categories. Then, you can combine your points when it comes time to redeem them.

Chase also lets you pool points with family members living in the same household. Ultimately, this makes it easy for you to work towards a common goal with a Player 2.

Related: Cards that Earn Chase Ultimate Rewards Points

Pay A Low Annual Fee

While we’d all love it if rewards cards came with no annual fees, the important question is whether you still get more value from the card than you pay in annual fees. At just $95 per year, the Sapphire Preferred’s annual fee is in line with other mid-tier travel cards — and it offers significantly more value.

Another great thing about the Sapphire Preferred is the ability to potentially upgrade it to the Chase Sapphire Reserve® (Rates & Fees). As you get more comfortable with annual fees, you can eventually determine if upgrading to the card is worth it based on how much value you get from its points and extra perks.

For many, the ability to earn Ultimate Rewards on everyday purchases can more than cover the cost of the card. However, the additional benefits you get just for being a card member do a great job of lessening the sting of the annual fee.

Enjoy Extra Perks and Benefits

The solid signup bonus and double points on dining and travel are fantastic incentives on their own, but the Sapphire Preferred has a whole bunch of additional perks and benefits.

It pays to read the Sapphire Preferred Benefits Guide as these benefits are a significant reason you want this card as a permanent feature in your wallet. The auto rental Collision Damage Waiver (CDW) and trip cancellation/interruption protection, in particular, are fantastic perks.

As an avid rental car renter, I have resorted to these protections multiple times and they have always come to the rescue. For example, I rented a car using my Sapphire Preferred, which ended up covering the damage to this vehicle after a smash-and-grab incident.

Bottom Line

If you’re ready to dive into the world of rewards points, the Sapphire Preferred is one of the best places to start. It combines a massive welcome bonus with an achievable spending requirement, strong earning rates, easy redemption options, and valuable travel protections — all for a low $95 annual fee.

Best of all, Chase Ultimate Rewards points are some of the most valuable you can earn. Even if you never get into complex redemptions, you can still get great value. And if you do decide to go deeper, your points have even more potential, thanks to Chase’s impressive list of transfer partners.

If you're looking for one of the best beginner travel credit cards out there, you really can’t go wrong with the Sapphire Preferred. And with a 100,000-point offer available, there’s no better time to apply than right now.

- Earn 100,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening.

- Enjoy benefits such as 5x on travel purchased through Chase Travel℠, 3x on dining, 3x on vacation homes, 3x on gas & EV charging, 3x on top streaming services and online groceries (excluding Walmart, Target, and wholesale clubs), 2x on all other travel purchases, 1x on all other purchases

- Earn up to $100 in statement credits each account anniversary year for hotel stays through Chase Travel

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Collision Damage Waiver, Lost Luggage Insurance and more.

- Get a year of complimentary Apple TV when activated by December 31, 2026 - a value of $156.

- Complimentary DashPass which unlocks $0 delivery fees & lower service fees for a min. of one year when you activate by 12/31/27. Plus, a $10 promo each month on non-restaurant orders.

- Receive one statement credit of up to $120 every four years as reimbursement for the application fee charged to your card for a Global Entry, TSA Precheck® or NEXUS application.

- Transfer points to leading airline and hotel loyalty programs

- Member FDIC

- 5X points on Lyft rides through September 2027

- 5X points on travel purchased through Chase Travel℠

- 3X points on dining at restaurants worldwide

- 3X points on gas and EV charging

- 3X points on vacation homes at top brands like Airbnb, Vrbo and more

- 3X points on eligible streaming services

- 3X points on online grocery purchases (excluding Target, Walmart, and wholesale clubs)

- 2X points on all other travel

- 1X point per dollar spent on all other purchases

For rates and fees of the cards mentioned in this post, please visit the following links: Chase Sapphire Preferred® Card (Rates & Fees), and Chase Sapphire Reserve® (Rates & Fees)