AwardWallet receives compensation from advertising partners when you visit our site, click on a link, when you are approved for a credit card, or when an account is opened. Terms Apply to the offers listed on this page. Enrollment is required for select Amex benefits. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers. Offers for Bank of America cards mentioned in this post have been updated as of 01/02/2025

Offers for the Bank of America® Premium Rewards® credit card and Citi Prestige® Card are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

Paying taxes is never fun. But if you need to pay the IRS anyway, paying your taxes presents a fantastic opportunity to earn points, miles, or cash back by using the right credit card. And with the lowest processing rate again set at 1.75% in 2026, you can actually profit from paying taxes with the right cash-back credit card!

Most Americans pay their taxes only once per year, around April 15. However, many self-employed and contract workers must make estimated quarterly tax payments throughout the year. The next payment period for these taxpayers is coming up on September 15, 2026.

In 2026, the IRS is partnering with only two payment processors again — down from three in the past. This is bad news for those of us who like to split tax payments across multiple credit cards to meet minimum spending requirements across several cards. Also, Pay1040 is still charging a much higher fee on business cards and all American Express cards.

In this post, we’ll cover everything you need to know about paying taxes with a credit card so you can build up those points balances.

Page Contents

What Is the Fee for Paying Taxes With a Credit Card?

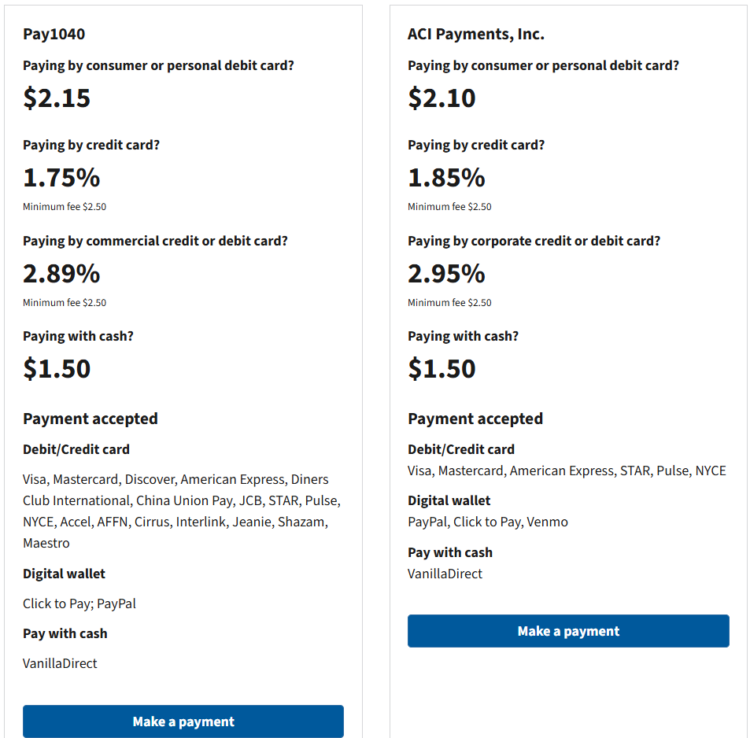

As outlined on the IRS website, taxpayers have two options to pay the IRS online with a credit card. Each payment processor charges a different fee for paying federal income taxes, depending on the type of card you use. The basic fee rate for personal cards is:

- Pay1040: 1.75% fee

- ACI Payments, Inc.: 1.85% fee

Both payment processors maintain a $2.50 minimum fee. And the IRS webpage now lists much higher fees when paying by “corporate credit or debit card”:

Also, the IRS no longer lists PayUSAtax as a tax payment processor. This is a bummer, as PayUSAtax previously offered the cheapest rates for paying federal taxes.

The IRS website also offers a table comparing debit and credit card payment processing fees assessed by each processor at various dollar amounts:

| Payment Amount | Pay 1040 - Debit Card Fee | Pay 1040 - Credit Card Fee | ACI Payments - Debit Card Fee | ACI Payments - Credit Card Fee |

|---|---|---|---|---|

| $50 | $2.15 | $2.50 | $2.10 | $2.50 |

| $100 | $2.15 | $2.50 | $2.10 | $2.50 |

| $250 | $2.15 | $4.37 | $2.10 | $4.62 |

| $1,000 | $2.15 | $17.50 | $2.10 | $18.50 |

| $2,500 | $2.15 | $43.75 | $2.10 | $46.25 |

| $10,000 | $2.15 | $175 | $2.10 | $185 |

Watch out for the minimum processing fees. If you pay $127 or less, you'll pay a higher processing fee rate than the 1.75%–1.85% rate listed. To pay the lowest rate of 1.75% through Pay1040, you'll need to pay at least $143.

Generally, you can expect two charges on your credit card statement. The tax payment may appear as “United States Treasury Tax Payment,” while the processing fee may be charged as “Tax Payment Convenience Fee” or “Service Fee.”

Will I be charged a cash advance fee for paying my taxes with a credit card?

Both payment processors (Pay1040 and ACI Payments, Inc.) confirm that the charge will be processed as a purchase and not a cash advance, so you won't have to worry about extra fees. With that said, you can always request that your card issuer lower your cash advance credit line low enough that you can be sure that the payment doesn't credit as a cash advance.

Maximizing Rewards With an IRS Credit Card Payment

The size of your federal tax obligation and the credit cards you have are two key components of approaching your tax payment. Taxpayers looking to maximize the rewards from their federal tax payment should consider the following strategies:

Earn a sign-up bonus when you pay the IRS with a credit card

In recent years, credit card sign-up bonuses have swelled in size. But so have spending requirements. Previously unheard-of 100,000-point sign-up bonuses are much more commonplace. However, some of these bonuses have very high spending requirements across a three-month period.

The offer on the Chase Sapphire Reserve® (Rates & Fees) offers a bonus that ticks a lot of boxes: 100,000 bonus points after you spend $6,000 on purchases in the first 3 months from account opening. Cardholders might not typically spend that much in a three-month period. However, a large income tax bill might boost spending enough to meet the bonus threshold.

For instance, putting a $6,000 tax payment on a credit card will cost around $105 through Pay1040. However, it can net 100,000 bonus points for new cardholders. The total points earned from such a purchase would be 6,000 + 105 + 150,000 = 156,105 points!

Even if you redeem these points for just 1 cent each, that's over $1,500 in value from this one payment! That's much more than the $105 processing fee paid. Plus, you can get much more value from these points by redeeming them through Chase transfer partners. For context, AwardWallet users tend to redeem Chase points at 2.02¢ apiece.

- Earn 100,000 bonus points after you spend $6,000 on purchases in the first 3 months from account opening.

- Get $3,000 in annual value with Sapphire Reserve.

- Earn 8x points on all purchases through Chase Travel℠, including The Edit℠ and 4x points on flights and hotels booked direct. Plus, earn 3x points on dining worldwide & 1x points on all other purchases

- $300 annual travel credit as reimbursement for travel purchases charged to your card each account anniversary year.

- Access over 1,300 airport lounges worldwide with a complimentary Priority Pass™ Select membership, plus every Chase Sapphire Lounge® by The Club with two guests. Plus, up to $120 towards Global Entry, NEXUS, or TSA PreCheck® every 4 years

- Get up to $150 in statement credits every six months for a maximum of $300 annually for dining at restaurants that are part of Sapphire Reserve Exclusive Tables.

- Count on Trip Cancellation/Interruption Insurance, Auto Rental Coverage, Lost Luggage Insurance, no foreign transaction fees, and more.

- Get complimentary subscriptions to Apple TV and Apple Music for a minimum of one year when activated by June 22, 2027, a value of $288 annually.

- Member FDIC

- 8x points on all purchases through Chase Travel℠

- 4x points on flights and hotels booked directly

- 3x points on dining worldwide

- 1x points on all other purchases

Hit a spending threshold by paying taxes with a credit card

For those not looking for a new credit card, there are still potential milestone spend levels that earn notable travel perks. For example, Hilton Honors American Express Surpass® Card cardholders earn a Free Night Reward after spending $15,000 on purchases on their card in a calendar year.

You can pay just $277.50 in fees to make a $15,000 tax payment through ACI Payments (Note: Pay1040 is charging a much higher 2.89% fee on Amex cards). The ability to earn a free night valid at almost any Hilton portfolio property worldwide at this price can be an absolute steal. Many of Hilton's luxury hotel properties charge rates two to three times higher than this processing fee per night.

Don't forget that you'll also earn 45,000 Hilton Honors points — worth around $261, based on recent AwardWallet user redemptions — on the purchase. That value alone almost covers the $277.50 cost of paying your taxes on this credit card.

Related: Why I Spend $15,000 Each Year on My Hilton Surpass Card

Pay taxes with a credit card that earns more points

Points and miles enthusiasts with no welcome bonus or spend threshold to meet should look to maximize the rewards from their expenses. Federal tax payments are no exception. Unfortunately, no credit card issuers offer a bonus category for paying taxes. Therefore, taxpayers should follow the same rules of thumb they typically follow for non-bonus spending.

For American Express Membership Rewards enthusiasts, The Blue Business® Plus Credit Card from American Express credit card will earn 2X Membership Rewards points on the first $50,000 of spend in a calendar year, then 1 point per dollar above that.

If you want 2x earnings with no cap, consider paying your taxes with the Capital One Venture X Rewards Credit Card or Capital One Venture Rewards Credit Card. Both cards earn an unlimited 2x Capital One miles on every purchase. Worst case, you can use miles at 1 cent each to pay for travel. That means you're getting at least 2% back on every purchase.

- Earn 75,000 Miles once you spend $4,000 on purchases within the first 3 months of account opening

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles on all other purchase

- Fee credit for Global Entry or TSA Pre✔® (up to $120)

- No foreign transaction fees

- $95 annual fee

- 5X miles per dollar on purchases through Capital One Entertainment

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases

Meanwhile, Chase loyalists have the potential to earn 1.5X Ultimate Rewards points by paying with the Chase Freedom Unlimited®. If you plan to use a Freedom Unlimited to pay your federal income taxes and redeem these points through the Chase Travel℠ portal, holding a Chase Sapphire Preferred® Card or Chase Sapphire Reserve® as well is key. Having either card will unlock the ability to transfer points to Chase Ultimate Rewards transfer partners.

Or Sapphire Reserve cardholders can redeem Ultimate Rewards points for up to 2 cents each through Chase's travel portal. Earning 1.5X points redeemable for up to 2 cents each means an overall spending reward of 3%. At a 1.25-cent redemption value, the spending nets a 1.875% return — which is just barely enough to cover the processing fee.

Alternatively, federal tax obligations might offer a great way to top up your points or miles balance. That can be especially helpful if you need to boost a specific hotel or airline program that's not available as a transfer partner of any of the major credit card issuers.

Collectors of Citi ThankYou® Points who hold both a Citi Double Cash® Card and a Citi Strata Premier® Card or Citi Prestige® Card card can earn 2X ThankYou® Points paying their taxes with their Citi Double Cash, which has no annual earning limits.

Earn cash back for paying taxes with a credit card

If you already have enough miles or are short on cash, points and miles may take a backseat. Instead, taxpayers might seek out the best available cash-back rewards from credit card spend. Thankfully, there are several credit cards that offer 2% or greater cash back on all purchases.

In addition to the aforementioned Citi Double Cash, the Capital One Spark Cash Plus also offers unlimited 2% cash back on all purchases. The American Express Blue Business Cash™ Card also earns 2% cash back on all eligible purchases on up to $50,000 per calendar year, then 1% (issued as a statement credit). Even using the payment processors with the highest 1.85% fee means those earning 2% cash back will come out ahead on their tax payment.

Those who hold the Bank of America® Premium Rewards® credit card can potentially earn even more than 2% cash back. While the card earns 1.5% cash back on general purchases, those with significant assets with Bank of America and related accounts earn up to a 75% bonus on these earnings, thanks to the Bank of America Preferred Rewards program. Cardholders with high enough savings can earn up to 2.625% cashback on their federal tax payments.

Given the $100,000 asset requirement to reach that reward level, this option isn't for everyone. But for those with enough savings, this is an incredible earning rate!

Related: All the Ways To Save When Doing Your Taxes

Other Benefits of IRS Credit Card Payments

Tax payments can be split between multiple credit cards. That can be especially helpful for those with high tax obligations. This provides taxpayers the opportunity to earn multiple credit card sign-up bonuses — perhaps one card apiece for those married filing jointly. Alternatively, you can split payments to reach the spending requirement on one sign-up bonus and then work toward a different credit card's spending threshold with the remainder of the payment.

You also can pay with a credit card to help manage cash flow. By paying your taxes with a credit card, you can delay the actual payment by a month or longer. For example, imagine a payment is made on the first day of a billing cycle. When the cycle closes a month later, cardholders generally have another month to pay the credit card “on time.” That means the funds are transferred out of your bank account a full two months after the date you made the tax payment.

Should I Pay Taxes With a Credit Card?

Paying taxes with a credit card can provide a (potentially considerable) net gain for taxpayers. But, two conditions need to be met. First, you need to be able to pay off (in full) the incurred credit card charge when it comes due. Second, the value of the rewards you earn from your payment should outweigh the processing fee.

It doesn't make sense to incur a 1.75% fee if you aren’t getting at least 1.75% worth of credit card rewards on the purchase. If you know which card to use to make a tax payment, you should have no trouble meeting this requirement.

Will you be paying income taxes with a credit card this year?

For rates and fees of the cards mentioned in this post, please visit the following links: Chase Sapphire Reserve® (Rates & Fees)