AwardWallet may receive compensation from advertising partners when you visit our site, click on a link, when you are approved for a credit card, or when an account is opened. Terms Apply to the offers listed on this page. Enrollment is required for select Amex benefits. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here’s our complete list of Advertisers.

Offers for the Amex EveryDay® Credit Card are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

There's a common misconception that lenders and credit providers will frown upon frequent applications and that applying for more credit cards will negatively affect your credit score. Luckily for award travelers, that isn't necessarily the case.

It's true — your credit score does take a temporary dip when you apply for new cards, particularly if you apply for more than one in a short period. Even so, provided you do other things to maintain healthy credit, like paying your credit card accounts on time and in full every month, adding more credit cards to your wallet can actually increase your credit score over time. Here's how.

Page Contents

How Are Credit Scores Calculated?

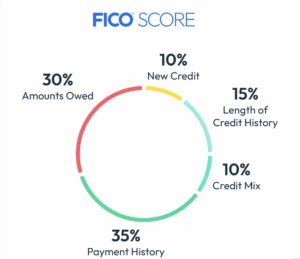

When we talk about a credit score, we are normally referring to your FICO® Score. Credit bureaus calculate your FICO Score using the following criteria:

- Payment history (35%): Late payments represent a much higher credit risk for lenders.

- Amounts owed (30%): Also referred to as credit utilization rates or available credit versus how much is in use.

- Length of credit history (15%): Average age of revolving debt accounts.

- New credit (10%): Hard pulls (credit inquiries from applications) and new accounts show here.

- Credit mix (10%): Ensure you have a diverse mix of credit, such as car loans, mortgages, guarantor accounts, and credit cards.

Another popular credit scoring tool is VantageScore, which puts different weights on similar categories:

- Payment history (40%)

- Depth of credit (21%)

- Credit utilization (20%)

- Balances (11%)

- Recent credit (5%)

- Available credit (3%)

As you can see, the categories are labeled differently, but they mean essentially the same thing. VantageScore places greater emphasis on payment history and the age of your credit accounts, while FICO gives more weight to your amounts owed, which is heavily influenced by your credit utilization ratio. VantageScore also separately considers your total balances and available credit, whereas FICO incorporates those factors into broader scoring categories.

Essentially, lenders want to see that you have a diversified credit portfolio over a sustained period, and that you're paying your bills on time and keeping your utilization rates low. If you tick all these boxes, credit providers are often more than happy to offer you new cards and financial products — or even increase your credit limit on existing cards — as you represent a “safe bet.”

We recommend keeping a close eye on your credit score. The vast majority of credit cards offer cardholders ways to check credit scores for free to monitor changes over time. Capital One offers CreditWise, American Express provides MyCredit Guide, Chase includes Credit Journey, and the list goes on and on. The name might change, but the function is the same. Cardholders get a quick and easy way to check their scores directly in their card accounts.

For a more detailed report, you can get a free copy of your credit report every week. There are also third-party services, like Credit Karma, that can help ensure cards and payments are updated correctly on your credit report. If anything unexpected comes up that is cause for concern, you can address it immediately.

Related: A Beginner’s Guide to Credit Scores — And How Credit Cards Impact Your Score

Why Do Credit Scores Dip When You Get a New Credit Card?

When you apply for a new credit card, the issuer performs a credit check, also known as a hard inquiry or hard pull. A hard pull gives the potential lender access to your credit report, which can help them decide whether to approve you for the card, how much credit you'll be extended, and the card's interest rate. These inquiries cause a small, temporary drop in your credit score.

Expect an immediate drop of two to five points per inquiry. However, this could be higher if you have limited credit or are applying for your first credit card.

Too many inquiries in a short time frame can cause a more pronounced dip in your credit score, so we recommend spacing out applications every six months or so. The dip in your credit score starts to fade within weeks of the application.

Typically, you'll see the impact from that inquiry fade within six months; at the 12-month interval, that hard inquiry likely has no impact on your credit score (depending on the exact scoring model and version used).

Related: Understanding Rewards Credit Card Application Rules and Restrictions

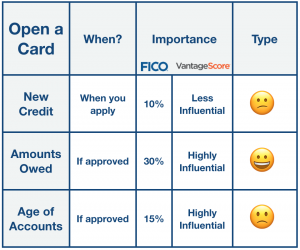

How Adding a Credit Card Improves Your Credit Score

Opening a credit card account can improve your credit score by lowering your credit utilization, diversifying your credit portfolio, and demonstrating your ability to manage revolving credit responsibly. These are all factors that play key roles in calculating your credit score.

Extend the length of your credit history

One key factor credit agencies look at when calculating your credit score is how long accounts have been open. Having just one or two new accounts open may count against your score initially. But over time, it adds to the overall length of your credit history, gradually increasing your credit score.

One of the reasons we recommend downgrading credit cards rather than canceling them outright is that long-standing credit lines can help improve your credit score. Opening a card now won't help in this area, but keeping it open for years to come will.

Reduce your credit utilization rate

Credit utilization plays a huge role in determining your credit score. Around a third of your credit score is calculated by your use of existing lines of credit, with lower utilization rates looked upon more favorably than high ones. So, how do more credit cards help lower your credit card utilization rate?

The more credit cards you have, the higher your total available credit. If you have a lot of available credit but your spending stays the same, your utilization rate will be low. Here's a simple example of how that could work:

- If you have one credit card with a $10,000 limit and you spend $3,000 per month, your utilization rate is 30% ($3,000/$10,000).

- If you get a second credit card with a $10,000 limit and still spend $3,000 per month, your utilization is now 15% ($3,000/$20,000).

- If you have five credit cards with $10,000 limits and still spend $3,000 per month, your utilization rate is now 6% ($3,000/$50,000).

Related: How To Manage Your Credit Score To Unlock the Best Travel Rewards

Bottom Line

So, does adding a credit card improve your credit score? Yes — as long as it's used responsibly and paid off in full each month. Rewards-earning credit cards can not only help push your credit score higher but can also provide access to amazing travel experiences for pennies on the dollar. And, higher credit scores mean you can be approved for more premium cards.