AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Editor note: Kennedy Miller is a 16-year-old writer and artist who has been writing and sharing her travel and financial wisdom since 2016 in publications including Business Insider and Points With A Crew. It’s never too early to start becoming financially savvy. In this post, Kennedy shares advice for her fellow teenagers about what to know and do to prepare to get their first credit card.

Credit cards can be very confusing. There are so many things to learn about them. Even though I personally don’t have a credit card, my family has taught me a lot about them and finance in general. I’m a teenager myself, but I already know a lot about credit cards. There are a lot of things to know, but I’m going to share my experiences and break it down for you.

What Teenagers Need to Know About Credit Cards

Credit cards are not free money. Just because you cannot see the money you’re using to pay doesn’t mean it’s not there. When you use a credit card, it’s like giving the bank an “IOU.” You’re saying that you will pay the bank back for this purchase later.

Another important thing to know about credit cards is that there’s a limit to how much you can spend. This is called a credit limit. If you go to that limit, it’s called maxing out your credit card. Maxing out your card is not a good thing. It means that you have more bills to pay, and it can really hurt your credit score.

What is a Credit Score?

One of the most important things about credit cards is their effect on your credit score.

A credit score tracks how often you pay your credit card and other bills on time. The more you pay on time, the better your score will be. Your payment history is the number one factor that makes up your credit score. Making late payments or missing payments lowers your credit score.

When you apply for new debt like a home mortgage, student loans, or car loans, the lenders will look at your credit score to see how reliable you are with paying your debt. If your credit score is good, you are more likely to get approved for the loan.

If your score isn’t very good, lenders might suspect that you aren’t good at managing your credit. That means you will be less likely to get approved for the loan. You might still be approved for the loan. However, the lender might charge a higher interest rate, meaning you will have to pay more money over the course of the loan.

Learn more: A Beginner's Guide to Building Healthy Credit

What Parents Can Do to Help

Navigating “adult stuff” can be really confusing for teenagers. It’s a good idea to ask your parents for help. After all, they’ve been doing this for a lot longer than you.

I think one of the best things parents can do to teach their teenagers about credit is give them opportunities to use credit in the real world. One way to do this is for your parents to add you as an authorized user on an established account.

When you’re an authorized user on someone else's card, it means your name is on the card, but you don’t have a legal obligation to pay the credit card bill. When your parents pay the bill, it will help establish a good credit history for you. On the other hand, if your parents pay the bill late, it might hurt your credit score.

What to Know about Interest

Do you think interest is interesting?

If you don’t, you probably should. Interest can be a part of your life for good or for bad. When you take out a loan, you have to pay interest if you miss a payment. If you keep missing payments, all that interest can add up to a lot of money — sometimes totaling more than your original payment.

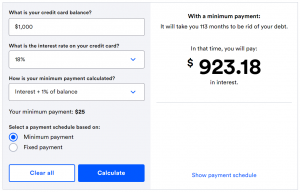

It’s always a good idea to pay your credit card bill in full, each and every month. You do have an option to only make the minimum payment. However, if you do that you might end up paying hundreds of dollars more before you pay off your purchase.

As one example, say you make a $1,000 purchase with a credit card that has an 18% interest rate. If you only make the minimum payment of $25 each month, it will take you more than nine years to pay off your debt. You’ll also end up paying over $900 dollars in interest in addition to the $1,000 purchase.

Interest isn’t all bad though.

If you put your money into a savings account, you can earn interest on your savings. Basically, the bank is paying you to put your money there. They want to use your money to make loans to other customers, so they’ll pay you with interest.

Learning about interest is a very important thing to know, because it is such a vital part of loans, and managing money.

How to Use a Credit Card Responsibly

Credit cards can be dangerous when not used responsibly. I understand that this can sound scary and make you afraid of using a credit card, but it’s really easy to learn about credit cards and how to use them properly. Credit cards are relatively simple — it’s just important to remember that credit cards don’t equal free money.

I like to think of credit cards not as just a little piece of plastic in my pocket. I think of them as actual money. This helps to keep me grounded. When I imagine actual money being there and having to pay it back later, it keeps me from spending unnecessary money.

Best Credit Cards For Teens

There are so many options for what kinds of credit cards to get. But some cards are specifically better for teens and first-time credit card applicants. Here are a few examples:

- Discover it® Secured Credit Card — Earn 2% cash back at restaurants & gas stations on up to $1,000 in combined purchases each quarter.. That's great for teens who are carpooling with siblings and eating out with friends. $0 annual fee.

- Capital One Platinum Secured Credit Card — This card is great for building credit, and it charges a $0 annual fee.

- Deserve EDU Mastercard — You don’t need to have a credit history to get this card, which makes it great for teenagers who are starting out

- DCU Visa® Platinum Secured Credit Card — Unlike many annual fee cards, this card doesn't charge fees when you use it internationally. Plus, you can add this card to Apple Pay, Google Pay, or Samsung Pay. However, not everyone is eligible to get this card.

The Bottom Line

It’s hard to be a teenager, and navigating the world of finance makes it even more confusing.

Credit cards can be your friend. If you know how to use them correctly, you can make them work for you. If you ever feel lost, talk to your parents or a mentor; they're here to help you transition into adulthood.

The comments on this page are not provided, reviewed, or otherwise approved by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.