AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

The days of applying for a U.S. credit card without supplying a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) when moving from overseas are ending. A new policy change means that, from August 23, 2023, you must provide a U.S. Social Security Number or ITIN when applying for a credit card and want your overseas credit history to be considered in the application process.

The change mainly affects Nova credit, which allows you to apply for U.S. American Express Cards and have your overseas credit history from select countries to be considered.

But why does this matter? Credit is “as American as apple pie,” as the saying goes. It affects everything from getting approved to move into an apartment to the rate you'll pay on a loan for buying a car or a house. Having good credit can affect many aspects of life in the U.S. Luckily, you might be able to use your credit history from another country when moving here, but the rules will get a little stricter soon. Here's what you should know.

What is Nova Credit?

Nova Credit is an American Express partner that allows you to transfer your international credit history when moving to the U.S. This means you don’t have to start from scratch in the U.S.; your previous history can be considered when applying for U.S. credit cards and financial service products.

Currently, you can transfer your credit history from the following countries:

- Australia

- Brazil

- Canada

- Dominican Republic

- India

- Kenya

- Mexico

- Nigeria

- South Korea

- Switzerland

- United Kingdom

At this point, you do not need a Social Security Number SSN or Individual Taxpayer Identification Number ITIN to apply for a U.S. credit card using this service. However, from August 23, 2023, you must supply either number when applying for a U.S. credit card. If applying for a card is on your to-do list, you may want to do so sooner rather than later.

How Credit Works

Essentially credit is a lender's risk appetite to lend you money. Credit scores (more about those later) are a way for financial institutions to assess whether:

- You can afford to repay what they are lending you.

- Your payment track record indicates that your finances are stable and that you can manage them promptly.

- How much of a risk you are for defaulting/not repaying the loan.

This is because credit cards in the U.S. (and most of the developed world) are a form of unsecured debt. If you default on your payments, it can be difficult for the bank to get its money back.

However, it's still possible to get credit cards in countries with less developed financial systems. However, in many cases, you must have a certificate of deposit with the bank for the equivalent amounts of your requested credit line. In that way, if you default, the bank already has access to a certificate of deposit to ensure they don’t lose out. It functions somewhat like secured credit cards in the U.S.

What Are Credit Scores?

Credit scores allow companies to assign a numerical value to the risk of extending you credit. As a rule, the lower the score, the higher the risk and the worse your credit. Conversely, higher scores mean you can manage your finances well and represent a low default risk for the bank.

Factors that determine your credit score

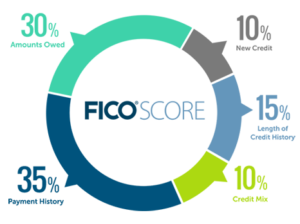

Most banks and credit lenders use a FICO score to assess your credit. It's composed as follows:

35% of your score is based on payment history, meaning you make on-time payments as required. 30% of your score is based on amounts owed, often called “debt utilization ratio.” This is a ratio of how much you owe against how much you're able to borrow (ex: If you have a credit card with a limit of $10,000 and have $5,000 of charges on it, your utilization is 50%.). These two factors alone account for nearly two-thirds of your credit score.

Other factors include having a mix of credit across multiple types, like car loans and credit cards (10% of your score), length of credit history (15% of your score), and how much of your credit is new (10% of your score).

One of the biggest myths about credit is that if you have no credit history, you should have good credit. “I've never owed anything, so my credit is good,” as the mentality goes. That's not true, though. The only way for lenders to assess your creditworthiness is to see your behavior with credit over time. That is why it pays to start early and establish a solid history of managing and dealing with credit successfully over time.

Vantage vs. FICO Credit Scores

Vantage and FICO are different methods with slightly different parameters and weightings used to calculate credit scores. One of the key differences between them is how they interact with the three major credit bureaus in the U.S.: Equifax, Experian, and TransUnion.

FICO creates a bureau-specific score, so your FICO score with TransUnion may differ from that with Equifax and Experian. On the other hand, Vantage creates a single model that can be used with a report from any of the three bureaus. But your FICO and Vantage scores are often different — maybe considerably.

What is a “good” credit score?

This can vary depending on whether you use a Vantage of FICO credit score model. As a rule of thumb, Vantage scores above 700 and Fico scores above 670 are considered good.

Related: Tips for Managing Your Credit Score

Building Good Credit

Building good credit is straightforward and is generally a matter of good habits and time. As a rule, if you consistently do the following, your credit should improve over time:

- Always pay your bill in full and on time.

- Never miss a payment.

- Don’t overextend yourself and borrow close to the maximum of your credit line. Only borrow what you know you can pay off within a reasonable period.

Over time, as you demonstrate that you can manage your finances well, your credibility with lenders will grow — and so will your credit score!

Related: A Beginner's Guide to Building Healthy Credit

Our Take

If you are moving to the U.S. (or recently moved) and were planning on applying for a credit card, the ability to do so without an SSN or ITIN was very convenient. It meant you could start immediately building your U.S. credit history. Unfortunately, the new policy means you will now have to wait until you have your SSN or ITIN number before applying for a credit card in the U.S.

Fortunately, there is still a window of opportunity through August 23, 2023, where you can apply without needing an SSN or ITIN. If applying for a US card is important or something you intended to do soon, you may want to do so now before the change.

Related: A Beginner's Guide to Building a Credit Card Application Strategy