AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Since early 2020, Bask Bank® has offered savers a mileage-earning savings account that earns American Airlines AAdvantage® miles instead of cash interest. For every dollar you deposit into your Bask Mileage Savings Account, you currently earn 1.75 AAdvantage® miles annually, with no cap on the number of miles you can earn each year.

If you don’t already have a Bask Mileage Savings Account, now is the perfect time to apply. Through August 31, 2026, Bask Bank is offering 20,000 AAdvantage® bonus miles to new account holders who deposit and maintain $50,000 or more in the account for 90 consecutive days.

Page Contents

Should You Earn Miles Instead of Interest?

During the low-interest-rate periods of 2020 and 2021, earning AAdvantage® miles on your savings was a no-brainer. Rather than earning less than 1% APY interest, you could earn AAdvantage® miles worth much more than one cent each.

Then, interest rates rose dramatically from mid-2022 to late 2023, making it a tougher decision between earning miles or cash interest. Now, the dynamic is starting to reverse. The Federal Reserve has lowered interest rates several times over the last year and indicated it would continue to do so.

That makes now a great time to revisit when it makes sense to earn miles instead of cash interest. Depending on your situation, keeping your savings in a Bask Mileage Savings Account can be “miles” ahead of holding your savings in a typical interest-earning account. Let's break down the math to help you determine which is better for your situation.

How Many AAdvantage® Miles Can I Earn On My Savings?

Bask Mileage Savings Account customers earn 1.75 AAdvantage® miles per dollar saved annually. And there's no cap on how many AAdvantage® miles you can earn. At current earning rates, you would earn 87,500 AAdvantage® miles annually if you deposit $50,000 into a Bask Mileage Savings Account.

And through August 31, 2026, new account holders can earn 20,000 AAdvantage® bonus miles by opening a new Bask Mileage Savings Account and holding $50,000 or more in the account for 90 consecutive days.

How does that stack up against earning interest in a typical savings account? Let's take a look.

Is Earning AAdvantage® Miles on Savings Better Than Earning Interest?

Before we dig into the math, remember that each person's situation is different. There may be situations where earning interest on a certificate of deposit or a high-yield savings account makes more sense than earning AAdvantage® miles.

With interest rates beginning to fall once again, the situation is changing quickly. A few high-yield savings accounts are still paying more than 4% Annual Percentage Yield (APY). However, given that the Federal Reserve has indicated that it will continue to lower interest rates, we can expect APYs for consumer savings accounts to decline as well.

Even at 4% APY, we can make a case for earning miles over interest; we think there are plenty of opportunities to get outsized value from your AAdvantage® miles, and the bonuses on offer present a unique chance to bank a huge number of miles on your savings.

Let’s consider a 4% APY savings account to illustrate the tradeoff between earning AAdvantage® miles and interest.

If you deposited $50,000 for 12 months, you would earn:

- 4% APY savings account: $2,000 in interest

- Bask Mileage Savings Account: 87,500 AAdvantage® miles

Valuing AAdvantage® miles

To get an accurate read on whether it’s better to earn miles or interest, we need to assign a value to those miles. AAdvantage® miles are commonly valued at around 1.7 cents per mile — although AwardWallet users average 2.56¢ per mile in actual redemptions.

As we show in the section below, it’s not hard to leverage AAdvantage® miles for better than 2¢ per mile in value. But, for calculation purposes, we’ll value AAdvantage® miles at 1.7¢ each, meaning the 87,500 miles earned on your $50,000 deposit would be worth roughly $1,500.

But isn't $2,000 cash interest better than $1,500 worth of miles?

The tax impact

Taxes are another important consideration. With a traditional savings account, your bank will issue a Form 1099 for the value of interest earned. At 4% APY on a $50,000 balance, you’d earn $2,000 in interest — all of which is considered taxable income.

Bask Bank will also issue a 1099 tax form for the value of AAdvantage® miles earned. Bask Bank has historically valued AAdvantage miles at just 0.42 cents per mile. While this value is subject to change, we’ll use that number for our comparison to the cost of earning traditional interest.

If you earn 87,500 AAdvantage® miles in your first year, you'll be taxed on $368 in income. You'll need to factor in your tax bracket to determine the amount you actually owe the government. The amount reported on your Form 1099-INT tax form is the additional income on which you owe tax — not the amount you will need to pay.

Running the numbers

Now that we have the pieces, let's walk through the after-tax value of earning cash interest vs. AAdvantage® miles for this example.

4% APY at a 35% marginal tax rate:

- 4% APY interest on $50,000 is $2,000 (taxable income)

- 35% of $2,000 is $700 (the amount you owe the government)

- Your net gain is $1,300 ($2,000 – $700)

Bask Mileage Savings Account at a 35% marginal tax rate:

- 87,500 AAdvantage® miles are valued at $368 (taxable income)

- 35% of $368 is $129 (the amount you owe the government)

- 87,500 AAdvantage® miles are worth $1,488 (using an assumed 1.7¢ per mile valuation)

- Your net gain is $1,359 ($1,488 – $129)

Comparing the two options, we get:

- Bask Mileage Savings Account: $1,359 (value of miles after deducting taxes)

- 4% APY savings: $1,300 (value of earnings minus taxes paid)

The argument for earning AAdvantage® miles is even stronger if you can redeem them for more than 1.7¢ each, if you have a marginal tax rate of more than 35%, or if you can't earn 4% APY.

On the other hand, you may prefer to earn cash interest if your tax rate is much lower or you aren't confident that you can redeem AAdvantage® miles for a high value.

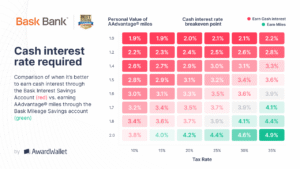

Here's a comparison of earning AAdvantage® miles vs. cash interest for a variety of mileage valuations and tax rate combinations.

Does the cash interest option win out in your situation? Check out the Bask Interest Savings Account, which is currently offering 3.75% APY.

Get Outsized Value From Your AAdvantage® Miles

Plenty of American Airlines redemption options offer better than 2¢ per mile — even when redeeming economy awards. Here are a few examples to demonstrate the kind of returns you can expect from your miles if you leverage American Airlines sweet spots, deals, or find the right routing and cabin-class combinations.

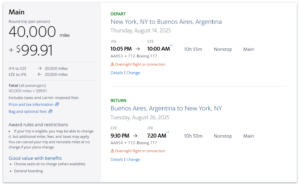

Round-trip Los Angeles to Buenos Aires in economy (2.45¢ per mile)

Using American Airlines' calendar function, you can find round-trip economy awards from New York (JFK) to Buenos Aires (EZE) from 40,000 AAdvantage® miles, plus a reasonable $100 in taxes.

Note that this award isn't in American Airlines Basic Economy. American Airlines awards book into Main Cabin — which offers the regular perks of choosing a seat and getting one free checked bag per passenger. Since American Airlines permanently eliminated fees to redeposit miles when canceling an AAdvantage® award, it makes more sense to book award tickets.

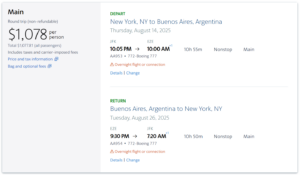

Comparatively, you'd need to pay $1,078 for Main Cabin economy cash flights on the same dates. That nets a redemption rate of 2.45¢ per mile ($1,078 – $100 in taxes = $978 / 40,000 miles = 2.45¢ per mile).

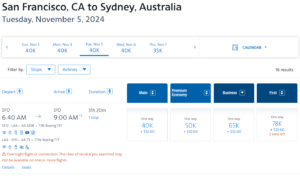

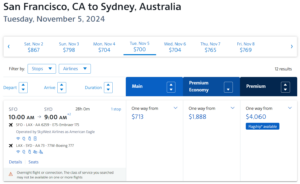

One-way international flight (e.g., San Francisco to Sydney)

Whether you're moving for work or piecing together a round-the-world trip, miles can provide a much better deal when you need to fly one-way internationally. Although American sometimes offers a small discount on round-trip award bookings, there's usually not much of a penalty for booking one-way awards.

Unfortunately, the same can’t be said for revenue fares, with one-way flights often dramatically more expensive when you pay cash.

In the example above, flying from San Francisco to Sydney will set you back 40,000 AAdvantage® miles, plus $32.60 in taxes. The cheapest cash alternative flight is $700 one-way, returning 1.67¢ per mile on an economy award ($700 – $32.60 in taxes = $667.40 / 40,000 miles = 1.67¢ per mile).

And that's just for an economy award. If you're considering paying for a premium cabin, miles get much more valuable:

- Premium economy: 50,000 miles + $32.60 taxes/fees vs. $1,888 = 3.71 cents per mile

- Business class: 65,000 miles + $32.60 taxes/fees vs. $4,060 = 6.2 cents per mile

- First class: 78,000 miles + $32.60 taxes/fees vs. $14,602 = 18.7 cents per mile

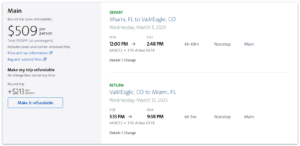

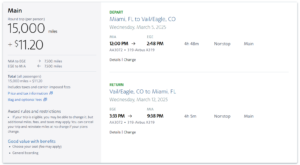

Round-trip Miami to Vail in economy (3.32¢ per mile)

You can find fantastic value with AAdvantage® miles, even on domestic awards. Again this winter, American Airlines is operating nonstop flights from Miami to Vail. On certain dates, cash rates aren't terrible, considering the premium route.

But you can get an even better deal with AAdvantage® miles, with round-trip awards starting at 15,000 miles plus $11.20 round-trip.

That nets a redemption rate of 3.32¢ per mile ($509 – $11.20 in taxes = $497.80 / 15,000 miles = 3.32¢ per mile). And this hot deal is during ski season.

We’ve saved this redemption for last, as we think it best highlights the benefits of earning miles over interest. Flying one-way to Tokyo from the mainland U.S. in Japan Airlines business class costs 60,000 miles plus $5.60 in taxes.

To purchase the same one-way itinerary would cost $7,136. That nets an incredible return of 11.88¢ per mile ($7,136 – $5.60 in taxes = $7,130.40 / 60,000 miles = 11.88¢ per mile).

For reference, 60,000 miles is what you'd earn by maintaining a $35,000 balance in your Bask Mileage Savings Account for 12 months — assuming no changes to the earning rate.

If you earn 4% APY interest on your $35k savings and have a 30% tax rate, your net gain after taxes would be around $980. Would you rather escape economy and experience one of the top business-class products in the world for 14 hours — or would you rather earn $980 cash?

There's no wrong answer. You just have to decide what's best for you.

Caveat: Consider how much you value business class

If you’re comparing the retail value of business class, things can get out of hand pretty quickly — especially with long-haul international flights. In some cases, it makes sense to use the price that you might actually consider paying for business or first class rather than the cash value of the ticket.

For example, if a flight costs $7,000+ to purchase in business class but you wouldn't pay more than $2,500 for the same flight, consider using that lower rate when calculating how much you're actually saving. Or consider the cost of an economy flight on that route if you wouldn't actually pay cash for a business-class ticket.

Final Thoughts

With the opportunity to earn a lucrative bonus of 20,000 AAdvantage® bonus miles — now available through August 31, 2026, this is the perfect time to consider opening a Bask Mileage Savings Account. If you can meet the $50,000 deposit requirement for this bonus and keep those funds in the account for 90 consecutive days, you could earn enough miles for a long-haul business-class flight.

And even a small deposit with Bask Bank can be a great way to supplement other miles-earning strategies. Since Bask awards AAdvantage® miles at the end of each month, even a small savings balance can generate the account activity needed to keep your AAdvantage® miles from expiring.

That's a much better return on your funds than earning interest in our book!

Terms & Disclosures:

Bask Bank is a division of Texas Capital Bank, Member FDIC.

Mile awards are subject to change at Bask Bank's sole discretion. Please see Terms and Disclosures for details.

American Airlines reserves the right to change the AAdvantage® program and its terms and conditions at any time with or without notice, and to end the AAdvantage® program with six months' notice. Any such changes may affect your ability to use AAdvantage® Rewards and Benefits that you have already accumulated. Unless specified, AAdvantage® miles earned through this promotion/offer do not count toward status qualification. American Airlines is not responsible for products or services offered by other participating companies. All third-party provider terms and conditions apply. For more information on miles and Loyalty Points, visit aa.com/loyaltypoints. For complete details about the AAdvantage® program, visit aa.com/aadvantage. For the AAdvantage® terms and conditions, visit AAdvantage® terms and conditions − AAdvantage® program − American Airlines.

American Airlines, AAdvantage®, the Flight Symbol logo and the Tail Design are marks of American Airlines, Inc.