AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Offers for the Capital One Spark Miles Select for Business are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

One benefit of Capital One miles is the ability to redeem them for any travel expense you charge to your eligible card. This includes everything from airfare to Uber rides, letting you reduce your travel expenses where it makes the most sense. Just charge an eligible travel expense to your card and apply miles toward it on Capital One's website.

Better yet, you have 90 days from the date of a travel purchase to cover it with miles. You can use Capital One miles earned with the Capital One Venture Rewards Credit Card, Capital One Venture X Rewards Credit Card, and Capital One VentureOne Rewards Credit Card to cover a travel charge you've already made — even if you didn’t have enough miles in your account at the time you made the purchase.

As long as you redeem within 90 days and earn enough miles during that time, you can use them to offset the cost. Let’s look at how to redeem Capital One miles to cover travel charges you’ve already made.

Page Contents

- Earn 75,000 Miles once you spend $4,000 on purchases within the first 3 months of account opening

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles on all other purchase

- Fee credit for Global Entry or TSA Pre✔® (up to $120)

- No foreign transaction fees

- $95 annual fee

- 5X miles per dollar on purchases through Capital One Entertainment (through 12/31/2025)

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases

Redeem Capital One Miles You Don't Have at the Time of Purchase

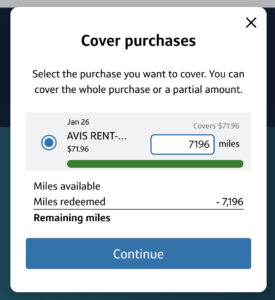

You can redeem Capital One miles at a fixed value toward travel purchases you've already made by requesting a statement credit to cover the charge. Buy any flight — or make another eligible travel purchase — and pay with a card that earns Capital One miles.

And you have 90 days to redeem miles toward that transaction. That means you don’t need to have all the miles in your account at the time of purchase. As long as you earn the miles within 90 days of the original charge, you’ll be able to redeem them.

Once the transaction posts to your account, you can redeem miles at 1 cent each toward the cost of travel. For example, redeeming 20,000 miles will knock $200 off the price of your flight or hotel stay. A credit will be posted to your account within a few days of making the redemption.

Unlike other types of fixed-value rewards, you don’t have to book through a specific website or worry about excluded vendors. If the purchase is categorized as travel on your credit card statement, you can redeem your miles to offset it.

Related: Do Capital One Rewards Miles Expire?

Buy Flights To Help Meet Minimum Spend and Redeem Miles for the Purchase Later

If you need to book a flight soon but don’t have enough points to cover the cost, opening a new Capital One credit card could make it happen. With the 90-day window to redeem miles for a purchase, you can:

- Apply for a card that earns Capital One miles, like the Capital One Venture card.

- Book your flight when the card arrives.

- Make other purchases to meet the minimum spending requirement to earn the card's welcome bonus (currently 75,000 bonus miles once you spend $4,000 on purchases within the first 3 months of account opening).

- Redeem the miles toward the flight cost after the welcome bonus posts to your account.

That way, the cost of your flight (or another travel purchase) can count toward the minimum spend to earn your bonus. Just note that you shouldn’t use this strategy unless you can afford to cover the cost upfront. Be sure to pay your credit card bill in full when your statement closes to avoid interest charges. Paying on time and in full is essential for building healthy credit.

The main advantage here is that you can buy a cash ticket using rewards you haven’t earned yet. Once your bonus posts, you can apply those miles toward the purchase before the 90-day window closes.

Related: How To Maximize Capital One Miles for Flights Within North America

Redeem Miles for Purchases Using the Sign-Up Bonus

A common question with this strategy is whether the sign-up bonus will post in time to redeem miles within the 90-day window.

Fortunately, Capital One typically awards miles as soon as eligible purchases post to your account — you usually don’t have to wait for your statement to close. This also applies to the welcome bonus. In most cases, it should hit your account shortly after you meet the spending requirement.

At worst, the bonus should post within a few days of your statement closing. So, in nearly every case, the miles should arrive well within 90 days of your purchase.

Things To Keep In Mind When Redeeming Capital One Miles

There are a few things you'll want to keep in mind before redeeming Capital One miles for a recent travel purchase:

- You don’t need to cover the entire purchase with miles. If your flight costs $1,000 and you only have 70,000 miles, you can still apply them to reduce your cost by $700.

- There is no minimum redemption amount.

- You can only get a statement credit for travel purchases made within the last 90 days.

- The merchant must code the purchase as ‘travel' for it to qualify for a statement credit.

That last bullet is pretty important. If the purchase doesn’t code as travel from the merchant, it won’t qualify. Here's how Capital One states that restriction:

“Purchases made from airlines, hotels, rail lines, car rental agencies, limousine services, bus lines, cruise lines, taxi cabs, travel agents, and time shares are generally considered to be travel purchases, and availability for redemption is based on the merchant category code assigned to them by the merchant. Capital One is not responsible for how merchants assign these codes.”

Related: The Best Capital One Credit Cards for Every Purchase

Cards That Earn Capital One Miles

We have a separate article covering all of the cards that earn Capital One miles in detail, but they're worth mentioning here. The bank offers personal and small business credit cards that earn Capital One miles.

Mileage-earning consumer cards:

- Capital One VentureOne Rewards Credit Card

- Capital One Venture Rewards Credit Card

- Capital One Venture X Rewards Credit Card

- 5 Miles per dollar on hotels and rental cars booked through Capital One Travel

- 5 Miles per dollar on purchases through Capital One Entertainment (through 12/31/2025)

- 1.25 Miles per dollar on every purchase, every day.

- 5X miles per dollar on purchases through Capital One Entertainment (through 12/31/2025)

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases

- 10X miles per $1 on hotels and rental cars booked via Capital One Travel

- 5X miles per $1 on purchases through Capital One Entertainment (through 12/31/2025)

- 5X miles per $1 on flights when booking via Capital One Travel

- 5X miles per $1 on vacation rentals booked via Capital One Travel

- 2X miles per $1 on all other eligible purchases

Capital One small-business mileage cards:

- Capital One Spark Miles for Business

- Capital One Spark Miles Select for Business

- Capital One Venture X Business

- 2X miles per dollar on every purchase, everywhere, no limits or category restrictions

- 5X miles per dollar on purchases through Capital One Entertainment (through 12/31/2025)

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- 5X Miles per $1 on purchases through Capital One Entertainment (through 12/31/2025)

- 1.5 Miles per $1 on every purchase.

- 10X miles per $1 on hotels and rental cars booked via Capital One Travel

- 5X miles per $1 on purchases through Capital One Entertainment (through 12/31/2025)

- 5X miles per $1 on flights booked via Capital One Travel

- 5X miles per $1 on vacation rentals booked via Capital One Travel

- 2X miles per $1 on other eligible purchases

It's also worth noting that if you hold a Capital One miles-earning card, you can combine the rewards earned with cash back cards like the Capital One Savor Cash Rewards Credit Card, Capital One Quicksilver Cash Rewards Credit Card, or Capital One Spark Cash and then transfer them to travel partners or redeem them to cover paid travel as outlined above.

Related: How To Get a Business Credit Card in 3 Steps

Final Thoughts

The ideal rewards strategy is building a portfolio of transferrable points, airline miles, and fixed-value rewards. Each type of point and mile has unique advantages and disadvantages. If you’re well-diversified, you can use the rewards that best suit your next booking.

In the case of fixed-value rewards, you’ll do best when paid airfare is relatively cheap or if the itinerary you want isn’t available as an award ticket. They can also help cover Uber or taxi rides, rental cars, and other miscellaneous travel expenses.

Frequent flyer programs typically require that you have enough miles in your account to cover the entire award price when making a booking. With up to 90 days to redeem Capital One miles retroactively, you can use the power of your future spending to earn the miles needed to cover trips you want to book now.

Although fixed-value rewards can't deliver the same kind of jaw-dropping deals you can get with a well-planned award ticket, their simplicity and flexibility are great reasons to add them to your points-and-miles arsenal.

What's your favorite way to redeem Capital One miles? Let us know in the comments below.

The comments on this page are not provided, reviewed, or otherwise approved by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.