AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Offers for the Capital One Spark Miles for Business and Capital One Spark Miles Select for Business are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

Capital One Miles is a latecomer to the flexible point currency world. The program only launched in 2018. Since then, the program has become one of the most valuable points currencies around, adding numerous transfer partners while still offering valuable, easy-to-redeem options.

If you've been building up a large balance of Capital One miles, you're likely invested in not losing your miles. As such, you might be wondering what situations could cause you to lose your Capital One miles. Specifically, you might wonder: “Do Capital One miles expire?” So, let's dive in.

Do Capital One Miles Expire?

Plain and simple: Capital One miles do not expire as long as your account is open. Per the Capital One Rewards page:

“Your rewards are yours for the life of the account—they will not expire. But if your account is closed, you may lose any cash back rewards you have not redeemed.”

So, if you are going to close your Capital One account, you must remember to redeem your miles before closing your account.

Track your points and miles expiration for 600+ loyalty programs and get email alerts before your miles expire by signing up for a free AwardWallet account.

Related: Top Ways to Redeem Capital One Miles for Travel Within the U.S., to the Caribbean, and More

What Happens to Your Capital One Miles If You Close Your Credit Card?

If you close a Capital One credit card, the rewards associated with that card are lost. So, if you are thinking of closing a Capital One card, you should redeem your Capital One miles beforehand to keep them from disappearing forever. You can use your miles in any of the following ways:

- Redeem to cover travel purchases made in the last 90 days.

- Transfer to one or more of the Capital One transfer partners (here's how to transfer Capital One miles).

- Redeem to book a trip through the Capital One Travel portal.

- Share your Capital One miles with friends or family who have a card that earns Capital One miles.

- Redeem to purchase gift cards from major retailers.

- Redeem your miles for cash, either as a statement credit or a check.

- Use your miles to pay for Amazon purchases.

- Redeem your miles through PayPal to pay for goods and services at millions of retailers online.

- Redeem for exclusive tickets and events through Capital One Entertainment.

Alternatively, you can transfer your miles to another Capital One account before closing your card. Note that this is different from my mention of sharing your Capital One miles with a friend or family member. If you have another Capital One card account, you may be able to transfer your miles from the account you want to close to another one of your Capital One accounts.

Related: Capital One Credit Card Offer History: Best-Ever Offers and When You Should Apply

Which Capital One Cards Earn Rewards?

Since Capital One miles do not expire as long as your account is open (and they're super valuable), you may want to focus on earning this type of reward. Several Capital One cards earn miles that can be transferred to 22 transfer partners. These include:

- Capital One Venture X Rewards Credit Card

- Capital One Venture Rewards Credit Card

- Capital One VentureOne Rewards Credit Card

- Capital One Venture X Business

- Capital One Spark Miles for Business

- Capital One Spark Miles Select for Business

$95

- 5X miles per dollar on purchases through Capital One Entertainment

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases

$395

- 10X miles per $1 on hotels and rental cars booked via Capital One Travel

- 5X miles per $1 on purchases through Capital One Entertainment

- 5X miles per $1 on flights when booking via Capital One Travel

- 5X miles per $1 on vacation rentals booked via Capital One Travel

- 2X miles per $1 on all other eligible purchases

$95

- 2X miles per dollar on every purchase, everywhere, no limits or category restrictions

- 5X miles per dollar on purchases through Capital One Entertainment

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Business Travel

Other Capital One credit cards earn cash back — which you can convert to miles if you also have a miles-earning Capital One card. A couple examples include:

- Capital One Savor Cash Rewards Credit Card

- Capital One Quicksilver Cash Rewards Credit Card

- Capital One Spark Cash

- Capital One Spark Cash Plus

$0

- 8% cash back on purchases made via the Capital One Entertainment ticketing platform

- 5% cash back on hotels, vacation rentals, and rental cars booked through Capital One Travel

- 3% cash back on dining and entertainment

- 3% at grocery stores (excluding superstores like Walmart® and Target®)

- 3% on popular streaming services

- 1% on all other purchases

$0

- 5% cash back on hotels, vacation rentals, and rental cars booked through Capital One Travel

- 5% cash back on purchases through Capital One Entertainment

- 1.5% cash back on every purchase, every day

$0 intro for first year;

$95 after that

- 2% Cash Back on every purchase

- 5% Cash Back on hotels and rental cars booked through Capital One Business Travel

Related: Capital One's Best Transfer Partners

Use AwardWallet to Track Your Capital One Miles

Even though your Capital One miles don't expire, it still pays to keep track of them using AwardWallet. That way, you can view all your points balances in one convenient place. This makes planning your travel rewards strategy much easier.

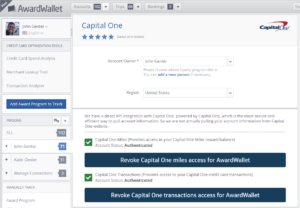

Tracking your Capital One miles is easy. All you need to do is log into your AwardWallet account and link your Capital One account in AwardWallet to get alerts anytime your rewards balance increases or decreases.

Related: How to Track Your Rewards Using AwardWallet

Our Take

The great news is that Capital One miles don't expire as long as your account remains open. That means you can focus on earning and maximizing the value of every mile you have. That said, if you are going to close your Capital One account, you need to remember to take steps beforehand so you don’t lose your hard-earned miles.

- Earn 75,000 Miles once you spend $4,000 on purchases within the first 3 months of account opening

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles on all other purchase

- Fee credit for Global Entry or TSA Pre✔® (up to $120)

- No foreign transaction fees

- $95 annual fee

- 5X miles per dollar on purchases through Capital One Entertainment

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases