AwardWallet receives compensation from advertising partners for links on the blog. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here's our complete list of Advertisers.

Offers for the Citi® Dividend Card and Chase Freedom Flex℠ are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

The Citi® Dividend Card is one of Citi‘s best cash back-earning credit cards. It's similar to cards like the Chase Freedom Flex℠ with its rotating quarterly bonus categories.

Each quarter, Citi announces up to three Citi Dividend categories where you can earn 5% cash back when you use your card. And enrollment is open for purchases from April 1 through June 30, 2026.

Here's how to enroll and get the most out of this unique card benefit.

Page Contents

Citi Dividend Card 5% Cash Back Key Terms

Like other cards with rotating quarterly bonus categories, the terms are simple: Activate the offer, use your card on eligible purchases within the quarter, and enjoy the rewards. The Citi Dividend Card is no different.

- Q2 2026 registration opened on March 12, 2026, for eligible purchases made from April 1 to June 30, 2026.

- Activate your bonus within your online account via this link.

- Earn 5% cash back on eligible purchases at qualifying merchants, up to a maximum of $300 per year.

It's worth emphasizing that: Unlike the Freedom Flex — where earnings are capped at $75 per quarter — the Citi Dividend Card limits cash-back earnings to $300 per year.

That means you can use it all in one quarter if you find a bonus category especially useful. However, once you have accumulated $300 in cash back, no matter how you earn it, you're done earning bonus cash back for the year.

Can I get the Citi Dividend card?

The Citi Dividend Card isn't currently open to new applicants, and it's not possible to product change your Citi card to this card. For those who have this card already, be sure to take advantage of these bonus categories — and make sure not to close or lose your account if you value carrying this card.

Related: Citi Credit Card Offer History: Best-Ever Offers and When You Should Apply

Citi Dividend Categories 2026 Second Quarter

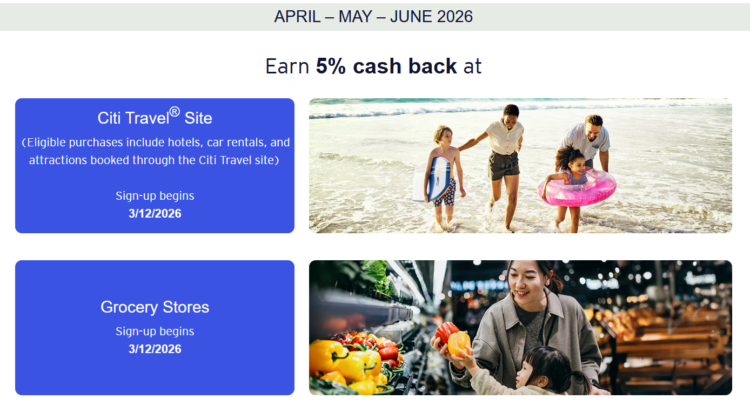

Registration just opened for the Citi Dividend 5% cash back categories for the second quarter of 2026. From April 1 to June 30, 2026, enrolled cardholders will earn 5% cash back on Citi Travel (excluding air travel) and at grocery stores.

Here are the terms of each category:

- Citi Travel Purchases: Excludes air travel purchases. Eligible transactions include hotel, car rental, and attractions only and must be booked through the Citi Travel site at CitiTravel.com or by calling 1-833-737-1288 (TTY:711). Citi Travel is powered by Rocket Travel by Agoda.

- Grocery Stores: Includes purchases at supermarkets, meat/seafood stores, dairy stores, bakeries, and miscellaneous food/convenience stores. Excludes purchases at general merchandise/discount superstores; wholesale/warehouse clubs; candy, nut and confectionery stores. Purchases made at online supermarkets or with grocery delivery services also do not qualify if the merchant does not use the supermarket merchant category code.

Citi Dividend Card 5% Cash Back History

One of the most observable trends throughout the Citi Dividend Card's cash back history is that many categories repeat. With rare exceptions, Citi has offered identical categories each quarter for the past several years. In other words, you should be able to plan ahead for your card purchases and ensure you max out the $300 cash back annually.

In the table below, you'll find each quarter's offerings dating back to 2021:

| Year | First Quarter | Second Quarter | Third Quarter | Fourth Quarter |

|---|---|---|---|---|

| 2026 | January – March • Amazon • Select streaming services | April – June • Citi Travel • Grocery stores | July – September • TBD | October – December • TBD |

| 2025 | January – March • Amazon • Select streaming services | April – June • Citi Travel • Grocery stores | July – September • Gas stations • Home improvement stores | October – December • Restaurants • Citi Travel |

| 2024 | January – March • Amazon • Select streaming services | April – June • Drug stores • Grocery stores | July – September • Gas stations | October – December • Restaurants • Citi Travel |

| 2023 | January – March • Amazon • Select streaming services | April – June • Drug stores • Grocery stores | July – September • Gas stations • Home improvement stores | October – December • Grocery stores |

| 2022 | January – March • Amazon • Select streaming services | April – June • Drug stores • Grocery stores | July – September • Gas stations • Home improvement stores | October – December • Restaurants • Select travel |

| 2021 | January – March • Amazon • Select streaming services | April – June • Drug stores • Grocery stores | July – September • Gas stations • Home improvement stores | October – December • Restaurants • Best Buy |

Alternatives to the Citi Dividend Card

If the Citi Dividend Card has piqued your interest, you might be disappointed to find it isn't open to new applicants, nor can you product change to it. Thankfully, there's a handful of other credit cards that earn a handsome amount of cash back on every or nearly every purchase.

Here's a look at three of our favorite cards for earning cash back with no annual fee:

- Wells Fargo Active Cash® Card (Rates & Fees): The Active Cash Card is a fantastic card that can put a lot of cash rewards into your wallet. It earns an unlimited 2% cash rewards on purchases, so there's no need to worry about annual or quarterly caps on the rewards you can earn. Learn more in our full review of the Active Cash Card.

- Chase Freedom Flex℠: The Freedom Flex is a formidable cash-back card, offering 5% on rotating bonus categories (up to $1,500 per quarter), 5% on travel purchased through Chase, 3% on dining at restaurants and drugstore purchases and 1% on other eligible purchases. If you max out your annual cash back in the quarterly categories, you'll put $300 back in your wallet every year. To learn more about this nifty product, dive into our Freedom Flex review.

- Citi Double Cash® Card (Rates & Fees): The Citi Double Cash doesn't have quarterly rotating categories and earns rewards as ThankYou® Points. But it's still a potent cash-back card. As a cardholder, you will earn 2% on every purchase with unlimited 1% when you buy plus 1% as you pay. Learn more in our Citi Double Cash review.

- Earn unlimited 2% cash rewards on purchases

$0

- Earn 5% on up to $1,500 on combined purchases in bonus categories each quarter you activate

- Earn 5% on travel purchased through Chase Ultimate Rewards

- Earn 3% on dining at restaurants, including takeout and eligible delivery services

- Earn 3% on drugstore purchases

- Earn 1% on all other purchases

- Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time.

Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

Related: The Best Cash-Back Credit Card Offers for Every Budget

Our Take

If you're among the lucky people still holding a Citi Dividend Card, activating the latest bonus and others when they come around is in your best interests. But given how useful the card's rotating categories are every quarter, it's entirely possible to max out your cash-back earnings in one three-month period.

For rates and fees of the cards mentioned in this post, please visit the following links: Citi Double Cash® Card (Rates & Fees)