AwardWallet may receive compensation from advertising partners when you visit our site, click on a link, when you are approved for a credit card, or when an account is opened. Terms Apply to the offers listed on this page. Enrollment is required for select Amex benefits. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here’s our complete list of Advertisers.

Offers for the Citi Prestige® Card are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

Note that some of the promotions mentioned in this post have expired. However, we still remain bullish on flexible point currencies right now due to low cash prices for travel.

With global travel plans on pause for many, hotels and airlines are doing everything they can to attract new business. We’re seeing especially generous promotions and some of the lowest prices in recent memory.

When the cost to buy travel with cash is lower than normal, your strategy for using rewards should change too. In our Facebook group, Award Travel 101, we discuss these topics daily. (If you haven’t joined yet, head on over and tell ‘em Joe sent you!)

Today, I want to share some insights from a recent Award Travel 101 conversation (check out the video) about flexible points—and why it's more important than ever that you know how to redeem them for maximum value.

Page Contents

What Are Flexible Points?

Flexible rewards are points or miles that give you more than one way to redeem. The most common ways to use points are:

- Cashback — Exchange your points for cash.

- Statement Credit — Use rewards to get reimbursed for a travel purchase.

- Travel Portals — Pay for travel with points (usually through a specific “portal” or travel website).

- Transfer Points — Move your flexible points directly to a partner airline or hotel loyalty program.

We cover each of these in much more detail in our beginner's post on the types of rewards points. With flexible rewards, you have the choice of more than one of the methods above. Most of the time, one of those choices is a lot better than the others.

In this post, I'll show you how to make the right decision every time.

Related: What Are the Best Flexible Rewards for Free Travel?

What is different in the COVID-19 era?

The conventional wisdom is that the fourth option—transferring points to other loyalty programs—is usually the best choice. When you see stories about using points for luxury travel like Emirates and ANA first class or Qatar QSuites, those redemptions often take advantage of transfer partners.

But right now, paid travel is cheaper than ever. And that means the other three ways to redeem your points are much more likely to be the right choice. Let’s take a look at some examples.

Using Flexible Points for a Hotel Stay

With borders closed to Americans, it's hard to get too excited about getting outsized value from overseas trips. However, flexible point currencies still quite valuable—just in a different way than before. That's because we have seen cash prices plummet for flights and hotels.

Let's start by assuming that you have two of the most popular types of flexible rewards:

- Chase Ultimate Rewards

- Capital One Rewards

Now is an especially good time to start collecting Chase Ultimate Rewards—thanks to the high-value welcome offers on the Ink Business cards.

- Earn 100k bonus points after you spend $8,000 on purchases in the first 3 months from account opening.

- Earn 3 points per $1 on the first $150,000 spent on travel and select business categories each account anniversary year. Earn 1 point per $1 on all other purchases

- Earn 5x total points on Lyft rides through 9/30/27.

- With Zero Liability you won't be held responsible for unauthorized charges made with your card or account information.

- Redeem points for cash back, gift cards, travel and more - your points don't expire as long as your account is open

- Go further when you book with Chase Travel℠. Enjoy competitive rates, seamless booking and premium benefits.

- Purchase Protection covers your new purchases for 120 days against damage or theft up to $10,000 per claim and $50,000 per account.

- Receive complimentary access to DashPass by DoorDash.

- Member FDIC

- 3X points per $1 on the first $150,000 spent in combined purchases on travel, shipping purchases, Internet, cable and phone services, advertising purchases made with social media sites and search engines each account anniversary year

- 1X point per $1 on all other purchases

- Earn 75,000 Miles once you spend $4,000 on purchases within the first 3 months of account opening

- 5X miles on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles on all other purchase

- Fee credit for Global Entry or TSA Pre✔® (up to $120)

- No foreign transaction fees

- $95 annual fee

- 5X miles per dollar on purchases through Capital One Entertainment

- 5X miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel

- 2X miles per dollar on all other purchases

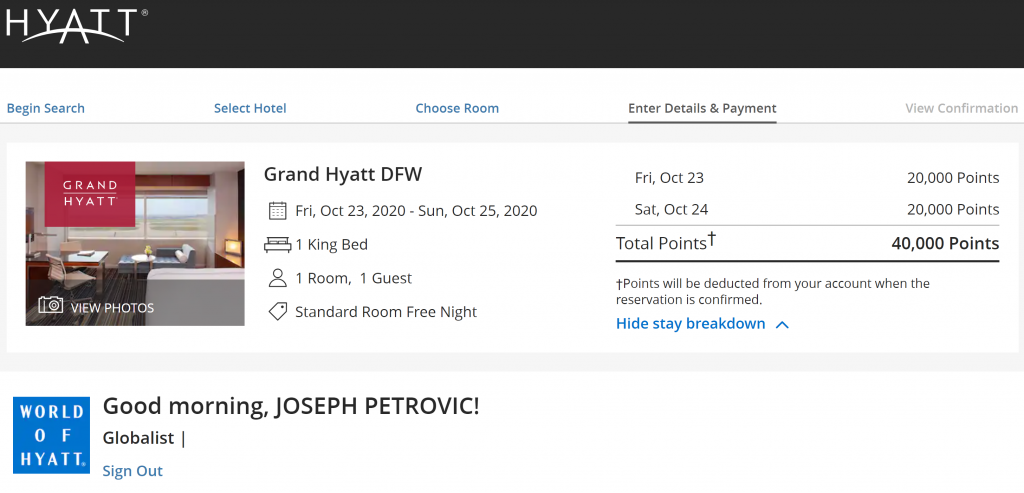

Take for example the following domestic travel hotel stay. An upcoming weekend getaway to Dallas, TX at the Grand Hyatt DFW—which is a Category 5 property located in the airport terminal.

1. Transfer Chase Points to World of Hyatt

Category 5 properties cost 20,000 Hyatt points per night. World of Hyatt is a 1:1 transfer partner of Chase Ultimate Rewards, so you'd need to transfer 40,000 Chase points for a two-night stay.

That means the 100,000-point signup bonus from the Ink Business Preferred® Credit Card would get you five nights at this excellent hotel.

But let's look at the other options to redeem points at this property.

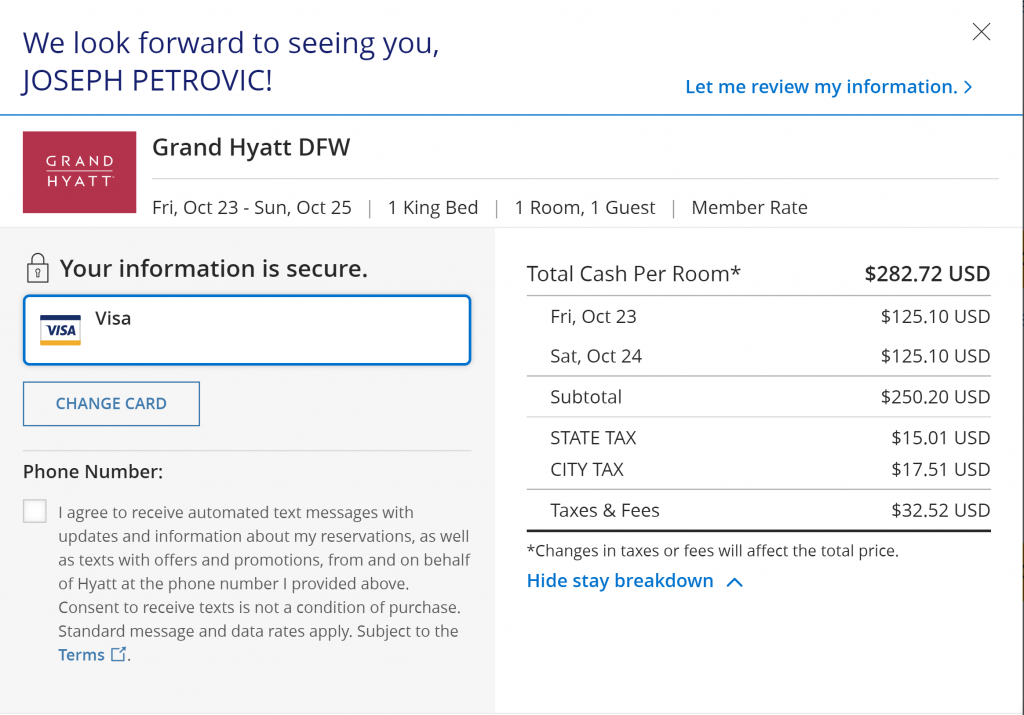

2. Redeem Chase Points Through the Chase Travel℠ Portal

Instead of transferring points directly to Hyatt, you can also redeem Chase points for a fixed value through the Chase Travel Portal. When the cash price is relatively low—like in this case—you'll spend fewer points with this method.

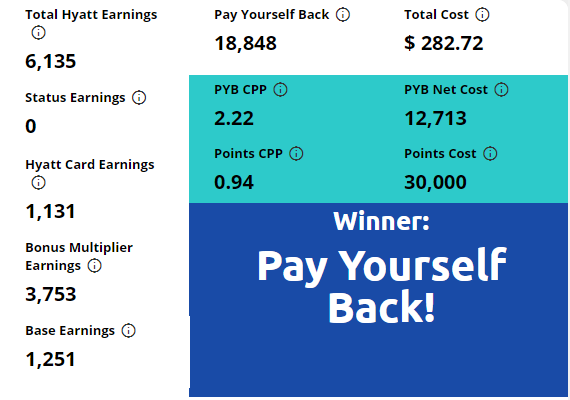

The value of each point depends on which Ultimate Rewards cards you hold, and the specific redemption. For example, a two-night stay for $282.72 would cost:

- 18,848 Ultimate Rewards points at 1.50 cents per point.

- 22,618 Ultimate Rewards points at 1.25 cents per point.

Related: How Much Are Points Worth in the Chase Travel Portal?

But there are a couple of major drawbacks to booking hotels through a third-party like Chase (rather than directly with Hyatt). First, you won't earn points from your stay. Hyatt's Bonus Journey's Promotion offered triple base points on paid stays booked through Hyatt (through February 28, 2021). That's 15 points per dollar spent!

Also, Hyatt doesn't award credit towards elite status or provide perks to elites unless you book direct.

3. Redeem Capital One Points for a Statement Credit

Capital One Rewards are the perfect solution if you care about earning Hyatt points and elite status. With Capital One, you aren't required to book through a third-party website like the Chase Travel Portal. Instead, you simply book your stay directly with Hyatt and pay with your Capital One Venture Rewards Credit Card.

Then, just redeem your Venture Miles within 90 days for a statement credit that cancels out the cost of your Hyatt stay.

- 28,272 Venture Miles would cover a two-night stay for $282.72

While this is more expensive than redeeming through the Chase Travel Portal, it might be a better choice after you account for Hyatt elite status, and the points you'll earn from your stay.

4. Pay Yourself Back with Chase (Available for a Limited Time)

Groceries are a necessary item in most of our budgets, where travel may not be. But, instead of using cash to buy groceries and points on travel, what if you were able to do the reverse? That's possible for a limited time thanks to Chase's Pay Yourself Back (PYB) tool.

There’s been plenty of buzz relating to this feature that Chase implemented as a part of their response to the COVID-19 pandemic. This option was originally valid through September 30, 2020, but it has recently been extended through September 30, 2021.

If you decided to use points to PYB, you’d be able to redeem your points at the same rates listed in “option 2” above. For example, $300 worth of grocery store purchases would cost:

- 20,000 Ultimate Rewards points at 1.50 cents per point.

- 24,000 Ultimate Rewards points at 1.25 cents per point.

Then, you could take that $300 and pay for your stay directly with Hyatt.

But there are other variables that could reduce it even further. Paying cash will allow you to earn points in the process too. In fact, with so many stackable promotions right now, we created a tool that can quickly determine whether you should transfer points to Hyatt or utilize the Pay Yourself Back feature. Here's our recent Facebook video with more info on the tool!

Using the example provided above, two nights would cost me just shy of 13K after returning over 6K points from the credit card, promotional offer, base earnings, and my Globalist status.

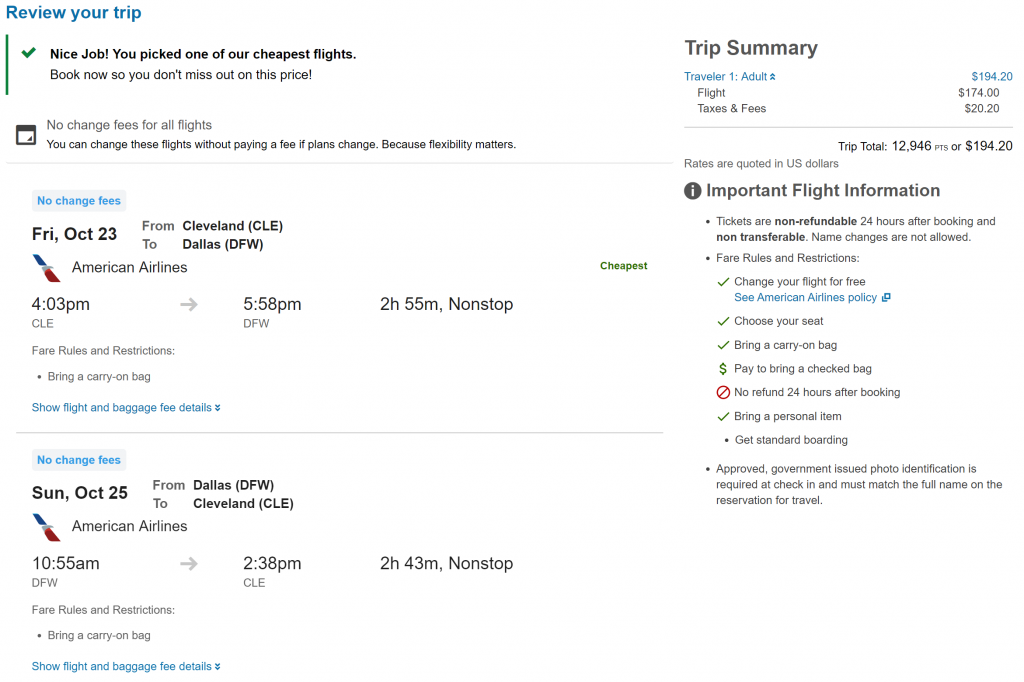

Using Flexible Points for a Flight

Flexible points can create the same opportunities with cheap airfare. Let's take a look at flights to Dallas for the same weekend. For this example, we'll add another flexible currency, Amex Membership Rewards to the mix.

(Terms apply)

- You may be eligible for as high as 100,000 Membership Rewards® Points after you spend $8,000 in eligible purchases on your new Card in your first 6 months of Card Membership. Welcome offers vary and you may not be eligible for an offer. Apply to know if you're approved and find out your exact welcome offer amount - all with no credit score impact. If you're approved and choose to accept the Card, your score may be impacted.

- Earn 4X Membership Rewards® points per dollar spent on purchases at restaurants worldwide, on up to $50,000 in purchases per calendar year, then 1X points for the rest of the year.

- Earn 4X Membership Rewards® points per dollar spent at US supermarkets, on up to $25,000 in purchases per calendar year, then 1X points for the rest of the year.

- New! Earn 5X Membership Rewards® points on prepaid hotel stays booked through AmexTravel.com or the Amex Travel App.

- Earn 3X Membership Rewards® points on flights booked through AmexTravel.com, the Amex Travel App, or purchased directly from airlines.

- Earn 2X Membership Rewards® points on prepaid car rentals booked through AmexTravel.com or the Amex Travel App and cruises booked and paid through AmexTravel.com.

- Earn 1X Membership Rewards® point per dollar spent on all other eligible purchases.

- Pay It® lets you tap in the American Express® App to quickly pay for small purchase amounts throughout the month and still earn rewards the way you usually do. Plan It® gives you the option to split up big purchases into equal monthly payments with a fixed fee. You'll know upfront exactly how much you'll pay.

- Updated! $120 Dining Credit: Earn up to a total of $10 in statement credits monthly when you pay with the Gold Card at Grubhub (including Seamless), Buffalo Wild Wings, Five Guys, The Cheesecake Factory, and Wonder. This can be an annual savings of up to $120. Enrollment required.

- $100 Resy Credit: Get up to $100 in statement credits each calendar year at over 10,000 qualifying U.S. Resy restaurants after you pay for eligible purchases with the American Express® Gold Card. That's up to $50 in statement credits semi-annually. Enrollment required.

- $84 Dunkin' Credit: Earn up to $7 in monthly statement credits after you pay with the American Express® Gold Card at U.S. Dunkin' locations. Enrollment required.

- $120 Uber Cash on Gold: Enjoy up to $120 in Uber Cash annually with your Gold Card. Just add your Card to your Uber account and you'll get $10 in Uber Cash each month to use on orders and rides in the U.S. when you select an Amex Card for your transaction.

- New! As an American Express® Gold Card Member, you can enjoy complimentary Hertz Five Star® Status. Enjoy benefits like skipping the counter at select locations, adding an additional driver at no additional cost*, and vehicle upgrades**. Benefit enrollment and Hertz Gold+ registration are required. *Additional drivers must meet standard rental qualifications and must be a spouse or domestic partner to qualify as complimentary. Other additional drivers subject to fees. **Benefits are subject to availability and vary by location. Additional Hertz program Terms and Conditions including age restrictions apply.

- Take advantage of a $100 credit towards eligible charges* at over 1,300 upscale hotels worldwide when you book The Hotel Collection through AmexTravel.com or the Amex Travel App **. *Eligible charges vary by property. **The Hotel Collection requires a two-night minimum stay.

- Book your travel through the Amex Travel App with added peace of mind - backed by American Express® service and support. Only for American Express® Card Members.

- Whenever you need us, we're here. Our Member Services team will ensure you are taken care of. From lost Card replacement to statement questions, we are available to help 24/7.

- No Foreign Transaction Fees.

- Annual Fee is $325.

- Terms Apply.

- 4X Membership Rewards® points at restaurants worldwide, plus takeout and delivery in the U.S. (on up to $50,000 per year in purchases, then 1X)

- 4X Membership Rewards® points at U.S. supermarkets (on up to $25,000 per year in purchases, then 1X)

- 5X Membership Rewards® points on prepaid hotels booked on amextravel.com

- 3X Membership Rewards® points on flights booked directly with airlines or on amextravel.com

- 2X Membership Rewards® points on prepaid car rentals booked through amextravel.com

- 2X Membership Rewards® points on cruises booked and paid through amextravel.com

- 1X on other eligible purchases

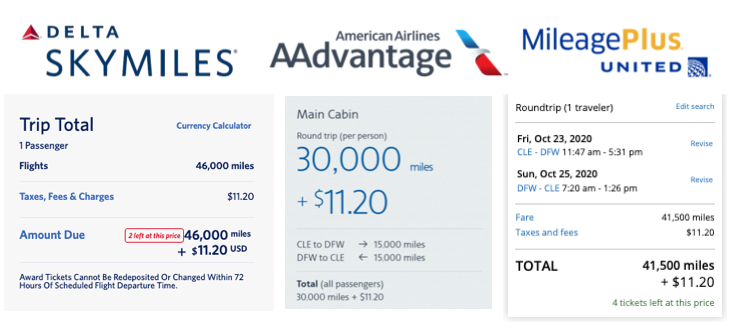

1. Transfer Points to a Frequent Flyer Program

If you decide to transfer miles, here is how the costs will break down:

- 46,000 Amex Membership Rewards – Transferred to Delta Skymiles

- 41,500 Chase Ultimate Rewards – Transferred to United Mileage Plus

You'll notice I didn't include a flexible-points price for the American Airlines option in the middle. Both Amex and Chase points can be transferred to British Airways Executive Club, and British Airways points are a great way to book short, nonstop domestic AA flights. (We've covered this in strategy in more detail here.)

However, to book those flights, you need American to offer AAdvantage® Saver award space. If AA.com were showing this flight priced at 25,000 miles for a round trip, we could book it using 18,000 British Airways Avios points—transferred from either Amex or Chase. But with the price at 30,000 miles, that option is off the table.

Related: Which Flights Can I Book with Miles?

2. Buy a Flight with Cash

Of course, there's the option to pay cash earning 5X on a card like the American Express Platinum Card® (on $500,000 of airfare purchases per calendar year booked directly with airlines) or the Citi Prestige® Card.

However, if we're trying to conserve cash, you could use the Capital One Venture to book direct with American Airlines. Just like in the previous example, you'd redeem your points for a statement credit after making your purchase.

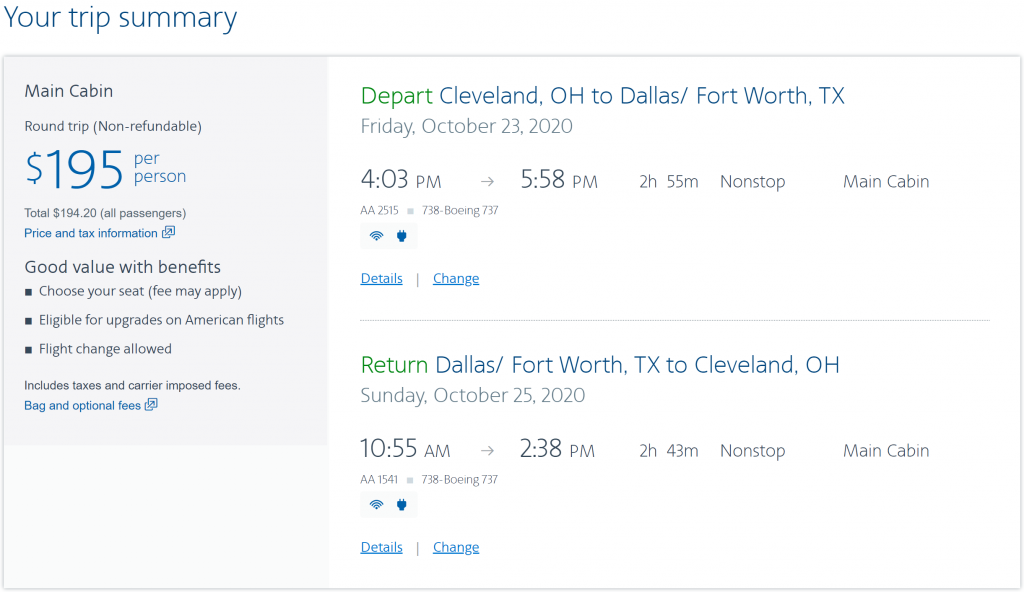

The flight above would cost:

- 19,420 Venture Miles — Redeemed for a statement credit with the Capital One Venture

Capital One has made huge strides in creating greater value for members by offering airline and hotel transfer partners. But in this case, “erasing” your charge is going to be the best option.

I'd much rather save my American Airlines AAdvantage miles for one of these higher-value awards. But is there yet another way that beats Capital One?

3. Redeem Points as Cash (Portal Booking)

Utilizing your Chase Sapphire Reserve® through the Chase Travel Portal, we can get an even better return on points.

You can also redeem Amex Membership Rewards points for 1.0 cents per point (Amex Travel® Portal). That would still be a lot cheaper than transferring Membership Rewards to Delta, but it doesn't measure up to booking with Chase.

With flights, you don't have to worry about earning elite status. Flights booked through third-party sites like Amex and Chase are still eligible to earn frequent-flyer miles and credit towards elite status.

Our Take

It's important to realize that not all award currencies are created equal. However, flexible point currencies such as American Express Membership Rewards, Citi ThankYou® Points, and Chase Ultimate Rewards provide us all with opportunities to do more for less! When you have multiple options, you are no longer at the mercy of the individual program.

Which program do you find to be most valuable?

For rates and fees of the cards mentioned in this post, please visit the following links: Ink Business Preferred® Credit Card (Rates & Fees), and American Express® Gold Card (Rates & Fees)