AwardWallet may receive compensation from advertising partners when you visit our site, click on a link, when you are approved for a credit card, or when an account is opened. Terms Apply to the offers listed on this page. Enrollment is required for select Amex benefits. The opinions expressed here are our own and have not been reviewed, provided, or approved by any bank advertiser. Here’s our complete list of Advertisers.

Offers for the Prime Visa are not available through this site. Some offers may have expired. Please see our card marketplace for available offers

Online shopping has become second nature for most Americans — a quick search, a few clicks, and your order is already on its way. But while most shoppers focus on price and convenience, there’s another way to save: shopping portals.

The right portal can turn an ordinary purchase into free cash back, bonus miles, or rewards that meaningfully accelerate your next redemption. But with dozens of portals, shifting payout rates, and complex rules for what does and doesn’t track, choosing the best option can feel overwhelming.

To make things easier, we put together a clear, practical guide to how shopping portals work, how to stack them for maximum returns, and which ones we trust the most.

Page Contents

What Is a Shopping Portal?

In a nutshell, shopping portals are a way to boost your savings or earnings when making online purchases. When a shopper navigates to a store's website after clicking a shopping portal and making a purchase, the store pays the shopping portal a commission. This commission is then shared in part with you, the shopper, in the form of cash back, points, or miles.

Depending on the store and the portal used, the shared commission can be as little as one bonus mile per dollar spent or as significant as several thousand bonus miles on a larger purchase. In either case, the earnings can add up quickly!

For this to work, however, you need to follow the correct process. Shopping portals rely on cookies/trackers in your web browser. Clicking through the shopping portal will take you to the store you want to shop at (Best Buy or Sephora, for example) and use trackers to see if you make an eligible purchase.

If you close your browser, navigate away from the page, or return several hours later to complete your purchase, you may not receive a payout from the shopping portal. You must follow the required link to be eligible for most portal bonuses, and some expire after an hour or two.

What Is Stacking?

“Stacking” is a beloved term in the points and miles community. It refers to the strategy of maximizing each purchase by layering multiple methods of earning and saving at once. Online shopping portals play a critical role in this strategy.

Remember, shopping portals earn revenue by referring customers to online stores. As such, any strategies to earn rewards or get discounts that don’t interfere with using a referral link from a shopping portal to reach the merchant's website can generally be combined for additional savings. Examples include:

- Redeeming a coupon or discount code on the merchant’s website

- Discounts, bonus points, or statement credits triggered by paying with a specific credit card, including Chase Offers or Amex Offers

- Points or cash back earned by using a rewards credit card to pay for your purchase

Related: If You Don't Stack, You're Wasting Money

Pay With the Right Rewards Card

The easiest way to get extra value from an online purchase is to pay with the right rewards card. There are two approaches to consider. The most common strategy is to maximize the points you earn on the purchase.

Optimize your rewards earnings

If your goal is to maximize your overall value, these three factors should guide your choice:

- Can you make progress toward earning a valuable reward by putting this spending on a specific card? If you’re working on the spending requirement to earn a welcome bonus, other factors like the number of points you’ll earn per dollar spent are less important.

- Do you have a card that earns extra points/cash back with this type of merchant? There are great cards for earning extra points on specific categories like travel, dining, or groceries.

- If you can’t earn extra points based on the category, the best option is to use a credit card that earns a solid return on all purchases. There are so many cards that are optimized for everyday purchases, so you'll never earn just one point per dollar or 1% cash back on your purchases. Several cards are optimized just for online shopping, too.

$0

- Unlimited 5% back at Amazon.com, Amazon Fresh, Whole Foods Market, and on Chase Travel purchases with an eligible Prime membership

- Unlimited 2% back on local transit and commuting (including rideshare)

- Unlimited 2% back at restaurants and at gas stations

- Unlimited 1% back on all other purchases

$0Rates & Fees

(Terms apply)

- 3% cash back at U.S. supermarkets (on up to $6,000 per year in eligible purchases, then 1%)

- 3% cash back at U.S. gas stations (on up to $6,000 per year in eligible purchases, then 1%)

- 3% cash back with U.S. online retailers (on up to $6,000 per year in eligible purchases, then 1%)

- 1% back on other eligible purchases

- Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit or at Amazon.com checkout.

- Earn unlimited 2% cash rewards on purchases

When to pay with a card that earns fewer points

There are three situations where you might be better off ignoring the advice above:

- If you need to earn a specific type of points for an upcoming trip. In this case, you might want to use a card that earns the points you need, even if you end up with fewer of them.

- If you can earn a bonus or statement credit by paying with a specific card. For example, if you're targeted for an Amex Offer that awards a statement credit on eligible purchases, you might want to use the card tied to that offer. You could save more money than the value of the lost rewards.

- If you're making a large purchase that might require purchase protection and extended warranty benefits. When purchasing a laptop or other big-ticket item, it can be beneficial to pay with a card that includes some of these benefits in case your new purchase gets damaged or stolen.

$95Rates & Fees

- 5X points on Lyft rides through September 2027

- 5X points on travel purchased through Chase Travel℠

- 3X points on dining at restaurants worldwide

- 3X points on eligible streaming services

- 3X points on online grocery purchases (excluding Target, Walmart, and wholesale clubs)

- 2X points on all other travel

- 1X point per dollar spent on all other purchases

$395

- 10X miles per $1 on hotels and rental cars booked via Capital One Travel

- 5X miles per $1 on purchases through Capital One Entertainment

- 5X miles per $1 on flights when booking via Capital One Travel

- 5X miles per $1 on vacation rentals booked via Capital One Travel

- 2X miles per $1 on all other eligible purchases

$595Rates & Fees

- 12X – Earn 12 Points per $1 spent on Hotels, Car Rentals, and Attractions booked on cititravel.com.

- 6X – Earn 6 Points per $1 spent on Air Travel booked on cititravel.com.

- 6X – Earn 6 Points per $1 spent at Restaurants including Restaurant Delivery Services on CitiNights℠ purchases, every Friday and Saturday from 6 PM to 6 AM ET. Earn 3 Points per $1 spent any other time.

- 1.5X – Earn 1.5 Points per $1 spent on All Other Purchases.

How to Find the Most Rewarding Shopping Portal

Whenever you make an online purchase, one of your first steps should be to check an aggregator tool. These websites help online shoppers maximize their spending by collecting all of the shopping portal offers or coupons in one place.

Two of the most popular websites for this purpose are:

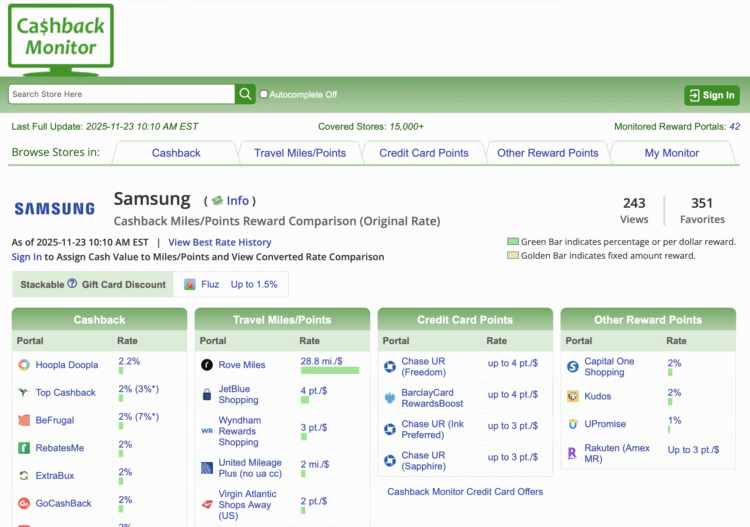

- Cashback Monitor: This website neatly displays the offerings of practically every shopping portal. This makes it easier to choose the portal that offers the best rewards.

- Evreward: Similar to Cashback Monitor, Evreward collects shopping portal offers as well as online store coupons, cash-back programs, and gift card bonuses.

Tips for Shopping Portals

Using any shopping portal is a reasonably straightforward process, but things can still go wrong. Between purchases not tracking or payouts registering at the incorrect rate, getting your promised commission can be a headache. To ensure that things go smoothly, we recommend following these steps:

- When using a shopping portal, always start with an empty cart. If there are already items in your cart from a previous visit, you risk not receiving the bonus miles for those items.

- Once you're on the merchant website, don't leave the window before checking out. Your original shopping trip was tied to the shopping portal, but a return visit may not be.

- Your web browser needs to have cookies enabled for portal bonuses to track.

- Always read the full terms of each bonus to ensure that the purchase you intend to make will qualify. What products are/aren't included? Do you have to spend a minimum amount? Look for these details.

- If possible, take screenshots throughout the buying process. That way, if things go sideways, you'll have proof of your purchase and portal use, as well as what you should earn.

- Follow up to make sure your earnings post. One important thing to keep in mind with any shopping portal is how long it can take to receive your payout. Earnings for travel bookings often won't post until after you complete your trip. So, make sure to follow up to ensure your earnings post.

Cash-Back Shopping Portals

Rakuten shopping portal

Rakuten is one of the oldest and best shopping portals on the internet. As such, its platform is among the most reliable in terms of commission and customer service. Better still, it maintains one of the best selections of partnered merchants and regularly offers lucrative referral/welcome bonuses to new customers — especially when you enroll through a referral offer.

Rakuten functions primarily as a cash-back portal. However, in early 2019, Rakuten launched a partnership with American Express and another partnership with Bilt Rewards in 2025. Now, Amex cardmembers can opt to earn Membership Rewards points instead of cash back on their purchases, just like Bilt Rewards members can elect to earn Bilt Points instead of cash back.

Depending on how you value Membership Rewards or Bilt Points, this has the potential to drastically improve your returns.

Related: How to Redeem American Express Membership Rewards Points — And Which Options Are Best

TopCashback

TopCashback is a site that has also been around for a while, originally launching in 2005. It offers lucrative cash-back rates that often match or beat competitors like Rakuten.

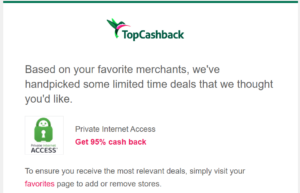

One nice aspect of TopCashback is the email alerts when favorite merchants and/or recommended merchants are offering increased earnings:

TopCashback payouts come in the form of PayPal, direct deposit, or, for an extra bonus, a gift card to a handful of stores.

Mr. Rebates

Mr. Rebates is a shopping portal founded in 2002. While it doesn't offer bells and whistles like in-store cash back or alternative payout options, it compensates with one of the widest selections of partnered merchants. Otherwise, it operates similarly to Rakuten or TopCashback. Again, the key is to double-check an aggregator to see which portal offers the best return.

Bank Shopping Portals

Barclays shopping portal

Barclaycard RewardsBoost offers certain cardmembers the ability to earn even more points than what they already earn through spending on their card alone. Rewards are deposited directly into your Barclays account.

Capital One Shopping

Earn cash back on purchases made through Capital One Shopping. Unlike Barclays, Capital One Shopping rewards do not earn award miles. Instead, they come in the form of cash back that can be redeemed for e-gift cards of your choice. You will need to set up an account to start earning cash back through Capital One Shopping.

Capital One Shopping even has its own Google Chrome browser extension, making it easier to guarantee you're getting cash back with each purchase.

Capital One Shopping is not to be confused with Capital One offers, which can earn miles or statement credits. You'll find these in your eligible Capital One account.

Chase Shop and Earn

Chase Ultimate Rewards are one of the most popular flexible rewards currencies in existence. Besides offering several valuable transfer partners, point collectors also can redeem points toward other travel purchases for up to 2¢ per point through the Chase Travel℠ Portal or as straight cash back at 1¢ per point.

Most people earn their Chase Ultimate Rewards points by spending on several popular credit cards, including:

- Chase Sapphire Preferred® Card (Rates & Fees)

- Chase Sapphire Reserve® (Rates & Fees)

- Sapphire Reserve for Business℠ (Rates & Fees)

But if your goal is to rack up Chase Ultimate Rewards points in a hurry, you owe it to yourself to check out Chase Shop and Earn.

As Chase's dedicated shopping portal, users can collect Ultimate Rewards points for every dollar spent at hundreds of online stores. If you stack this with your earnings from using a great everyday spending card like the Freedom Unlimited (Rates & Fees), it's possible to significantly increase your Ultimate Rewards balance after only a few purchases.

Airline Shopping Portals

Several airlines have branded shopping portals. Here's a look at a handful of our favorite ones.

Alaska Airlines Atmos Rewards Shopping

Alaska's Atmos Rewards Shopping portal includes popular brands like Walmart, Home Depot, Best Buy, and Kohl's, typically offering between 0.5–5 points per dollar spent.

Alaska also offers a handy Google Chrome Extension to automate the process. Moreover, the portal often features raised bonuses for meeting specific shopping criteria. Keep an eye on our current shopping portal bonus post so that you can time your purchases to coincide with new member bonuses or elevated earnings.

American AAdvantage® eShopping

American Airlines operates its shopping portal, called AAdvantage eShopping. It offers AAdvantage members a way to accelerate their AA earnings through normal online purchases.

As you might expect, it functions much like other shopping portals. However, instead of earning cash back, you'll earn AA miles and Loyalty Points.

The portal regularly offers increased bonus opportunities, as well as the ability to automate your portal earnings with a Google Chrome Extension. You can even earn AAdvantage elite status purely from taking advantage of the shopping portal — no flying required — thanks to the ability to earn Loyalty Points on most purchases.

Related: Playing the American Airlines Loyalty Points Game

Delta SkyMiles Shopping

SkyMiles Shopping is Delta's shopping portal, offering lucrative earning rates and bonuses to SkyMiles collectors. Similar to other airline portals, you need to create a separate account to utilize it. On the plus side, it's possible to look through earning rates without signing in.

JetBlue TrueBlue Shopping

JetBlue's TrueBlue Shopping is a great way to earn TrueBlue points on regular purchases. The portal functions like any other airline shopping portal. However, it also offers one additional feature: card-linked offers.

In addition to online shopping, JetBlue offers a way to earn bonus points for in-store purchases. TrueBlue members can register an eligible card and receive bonus points for purchases made with partnered merchants.

Southwest Rapid Rewards Shopping

Southwest's shopping portal, Rapid Rewards Shopping, is virtually identical to portals of Alaska and American Airlines. It offers bonus Rapid Rewards points for purchases at 1,100+ merchants. It also offers a browser extension button for Google Chrome, ensuring you're getting points with each purchase.

The real selling point for Rapid Rewards Shopping is the fact that bonus points count toward Companion Pass qualification. This means that you're not just earning extra points; choosing Southwest's portal for your online shopping can help you achieve one of the most valuable perks in the airline industry.

United MileagePlus Shopping

United MileagePlus Shopping is one of the better airline shopping portals available. Not only does it maintain lucrative bonuses at over 1,100 stores, but it also offers card-linked bonuses for in-store purchases and a Google Chrome Extension to automate your earnings. Plus, if you hold a United credit card, you can earn even more.

Additionally, United MileagePlus Shopping regularly offers a bonus for new users. Lastly, United MileagePlus Shopping regularly introduces limited-time offers for meeting certain purchase criteria. Keep an eye on our post for shopping portal bonuses for all current offers.

Related: United MileagePlus X App: Earn Extra United Miles From In-Store Purchases

Hotel Shopping Portals

Hotel shopping portals aren't as prevalent as airline shopping portals. However, one of our favorite hotel shopping portals offers Wyndham Rewards points, which you can put towards interesting redemptions, such as vacation rentals.

Wyndham Rewards shopping portal

Just like the other shopping portals, you can shop through hundreds of online retail stores and services with the Wyndham Rewards shopping portal.

The main difference is you are earning Wyndham Rewards points on your purchases instead of airline miles. There also don't appear to be as many promotions as the airline shopping portals have, although there is the occasional offer to earn bonus points on your purchases in the shopping portal. New member bonuses also can help you earn extra points when signing up.

Transferable Rewards Shopping Portals

Last but not least, there's one portal that earns transferable miles on purchases at participating retailers: Rove Miles.

Rove Miles shopping portal

Rove Miles is a relative newcomer in the points and miles world, and it's more than a hotel and flight booking portal. It also lets you earn transferable miles on your online shopping.

If you haven't signed up for Rove Miles yet, you can earn bonus miles by joining this free program through a referral link. With the right mix of online shopping, hotel stays, and flight bookings, you can build a sizable balance of Rove Miles that you can later transfer to 18 travel partners.

Final Thoughts

One of the pillars of award travel is to maximize every purchase you make. When making a purchase online, a shopping portal is one of the easiest ways to do so.

While the sheer number of shopping portals can understandably cause analysis paralysis, the key is to always have a plan. Ask yourself the following questions:

- What points or miles do you need for your next redemption?

- Which points are the most difficult to collect otherwise?

- What other stacking options are available for this transaction?

The answers to these questions will give you a good starting point for which portal you should consider. Then, use an aggregator (like CashBackMonitor) to see which portal offers the best return for your impending purchase. A couple more clicks, and you're well on your way to earning tons of points.

Ready for more? Check out our guide to dining rewards programs.

For rates and fees of the cards mentioned in this post, please visit the following links: Blue Cash Everyday® Card from American Express (Rates & Fees), Chase Sapphire Preferred® Card (Rates & Fees), Citi Strata Elite℠ Card (Rates & Fees), Chase Sapphire Reserve® (Rates & Fees), and Chase Freedom Unlimited® (Rates & Fees)